We recommend products that we love. When you buy through links on our site, we may earn an affiliate commission.

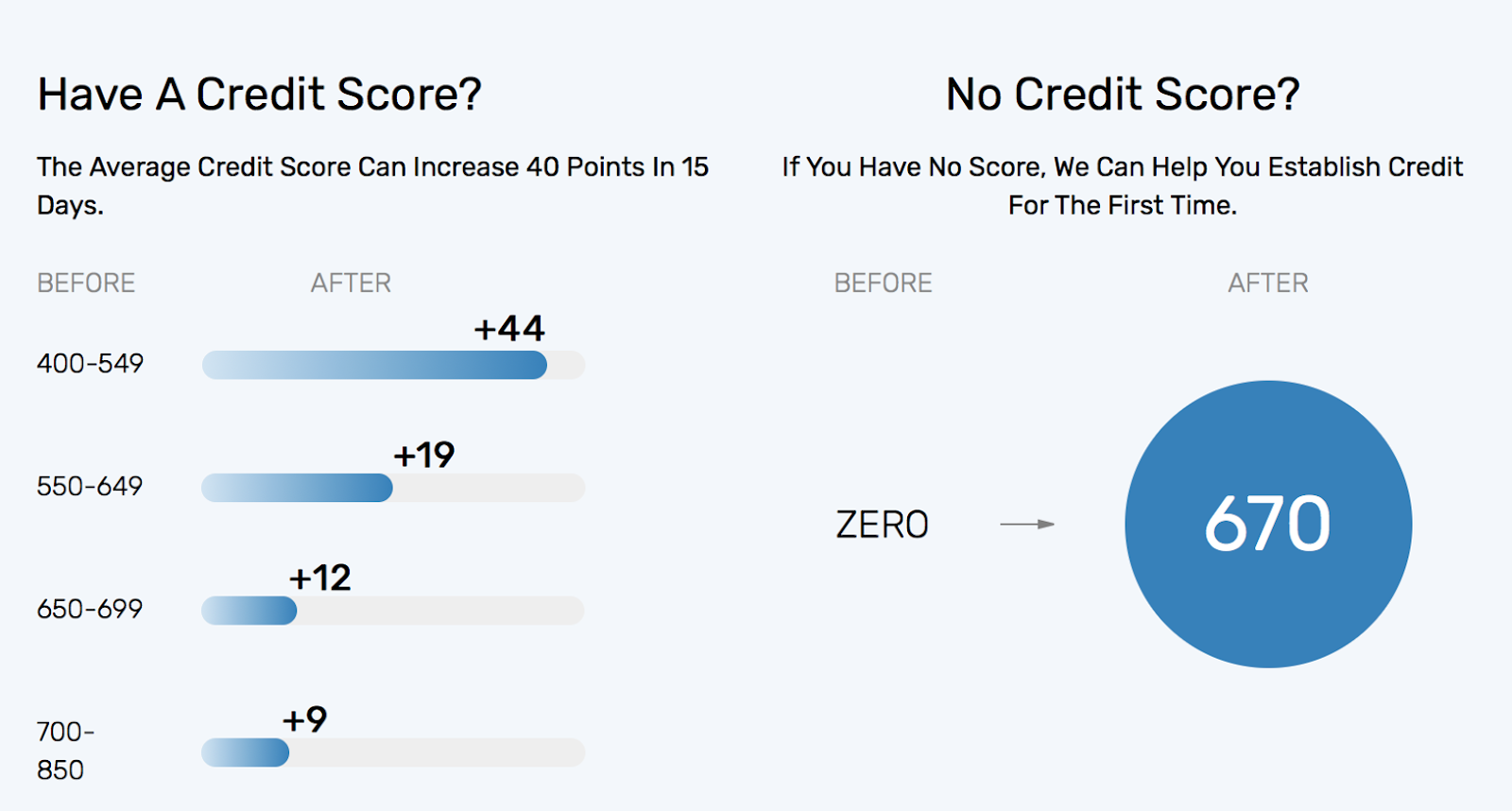

Adding a tradeline to your credit report can significantly boost your credit scores. A single credit score could be easily increased by 20-100 points! Although, the exact point increase will depend on the current state of your credit reports and what kind of tradeline you are opening.

When you are looking to add a tradeline to your report(s) in order to improve your score, one of the most common go-to’s is purchasing credit card authorized user slots. Doing this can quickly boost your credit history and credit scores.

But becoming an authorized user is not the only way to add a new tradeline to your credit. There are actually many ways to add tradelines to your credit. For example, opening a new credit account is one way, and reporting your rent payments is another.

So before you run out and purchase an authorized user tradeline, let’s take a look at how tradelines can improve bad credit and which tradelines are the best.

What Happens When You Add Tradelines to Your Credit?

A tradeline is any account that appears on your credit report. This can include:

- Credit cards

- Personal loans

- Auto loans

- Mortgage

- Line of credit

- Rent payments (if reported to the credit bureaus)

- Utility payments (if reported to the credit bureaus)

Each of the credit lines, or tradelines, that you have showing up on your credit reports includes a specific set of information that influences the five aspects of your credit score; payment history, amounts owed, length of credit history, credit mix, and new credit.

When you add a new tradeline to your credit, this will impact many of those aspects.

For instance, let’s say you open a new credit card. This will immediately impact the new credit portion of your score as this factor looks at credit inquiries and new accounts.

The newness of the credit card account will also impact your length of credit history. This factor is calculated by tallying up the average age of your accounts.

So if you have three accounts with two of them being two years old and a new one at one-month-old, your average age of account would be 16 months.

24 months + 24 months + 1 month / 3 = 16.3 months

The credit limit on that new card would also likely impact your credit utilization. Your credit utilization is a significant part of the amounts owed portion of your score. It is determined by totaling up your available credit and comparing it to your reported balances.

So if you added a new account with a high limit and a low balance, it could dramatically decrease your credit utilization ratio. And the lower your utilization, the higher your credit score.

Adding a rental or utility payment tradeline will impact your credit score differently.

Since these tradelines don’t report a credit limit, they won’t impact your amounts owed. But having your past payments reported could positively impact your payment history and length of credit history. Here is a list of tradelines to build credit if you’re interested.

Is Buying Authorized User Tradelines Legal?

Currently, there are no laws against buying or selling authorized user tradelines. But there is no guarantee that laws won’t be introduced in the future. This is partly because the credit card companies, credit bureaus, and FICO hate this practice.

For a credit card company, the practice of selling someone your authorized user slot is expressly forbidden in their terms of service. So proceeding with this action will be viewed as fraud and could result in the closure of your account.

FICO has been cracking down on the buying tradelines part. Their more recent credit scoring models (9 and 10) all look for these fraudulent authorized user accounts on your credit reports and remove them from their score calculations.

So even if you purchase a seasoned tradeline slot from someone with good credit, it may not improve your score if the FICO scoring model flags it as fraud.

Another considerable risk with buying tradelines is the potential for disaster. You can’t control what the primary cardholder does. So if they begin carrying a larger balance or accrue late payments, your credit could be damaged.

Tradelines You Can Buy that Are Legal and Effective

Instead of resorting to the shady process of buying authorized user tradelines, opening a primary tradeline will be cheaper, better for your credit score, and much less risky.

Below are five of our favorite tradelines that are good for credit repair and easy to get even if you have bad credit.

CreditStrong

CreditStrong offers an installment loan tradeline that even those with poor credit can qualify for.

There is no credit check for any of the loans CreditStrong provides. This makes this account a relatively easy tradeline to add to your credit report.

All of CreditStrong’s credit builder loans are secured installment loans that also act as savings accounts.

Let’s say you are approved for a $1000 loan. Instead of giving you the funds upfront, CreditStrong places the $1000 in a locked savings account. Then, each month you make your monthly loan payment, you will unlock a portion of your loan funds.

CreditStrong will release the full loan funds to you minus any admin fees at the end of the repayment term, which can range from one to 10 years.

This can allow you to build your savings as you increase your credit score. In fact, according to CreditStrong, their average customer sees a 70 point increase to their credit score with just 12 months of on-time payments!

And those who start with no credit score see their credit score rise to the mid 600s within 12 months.

Self

Self is another company that offers a no credit check credit builder loan.

Much like CreditStrong, Self’s loans are secured loans, with the collateral being the loan funds themselves.

No credit check means that their loans are easy to qualify for, and even if you don’t get approved, there is no damage to your credit for applying.

While Self doesn’t offer as broad of a selection of loan amounts compared to CreditStrong, they do offer a co-branded credit card.

This credit card account is actually tied to your credit builder loan. It is a secured credit card that uses funds from the unlocked portion of your credit builder account as a security deposit.

So, if you took out a $1000 loan and had $300 of it paid off, you could transfer up to $300 of your loan funds to your secured credit card as a deposit.

Having two reporting accounts tied to one collateral fund can allow Self’s customers to build their credit twice as fast. According to a recent study by Self, their average loan customer experienced a 32 point credit score increase by the end of repayment term (1-2 years).

Their Visa card is newer, and there are no statistics yet for average credit score increase. Still, we can assume the credit score increase will be higher for those utilizing both the loan and credit card products.

Extra Debit Card

Extra is an account that reports like a revolving tradeline but operates like a debit card.

Your credit won’t be checked when applying for the Extra card. Instead, you’ll need to link your checking account. Extra will then look through your spending habits to determine your “Spend Power”, which is like a credit limit.

Each time you use your Extra card to make a purchase, Extra will cover that purchase price. By the next business day, they will then draw money out of your linked checking account to repay themselves for that purchase.

This means that you cannot carry a balance on the card, there are zero interest fees, and your credit limit essentially resets every day.

Extra then reports your purchases as payment activity to Equifax and Experian at the end of the month.

This allows you to build credit similar to a traditional credit card.

Extra is a newer product on the market, and the company behind it has not yet published any stats on the average score increase their customers see. But, the customer reviews they cite on their webpage show customers with credit increases of 30 points or more.

BoomPay

The BoomPay app offers an entirely different kind of tradeline, rental payments.

Qualifying for a new credit tradeline with a poor credit score or limited income can be nearly impossible. But if you are currently paying rent, you can have your payment history reported to the credit bureaus for a small fee.

The BoomPay app links directly to your landlord’s payment portal, or if your landlord doesn’t offer one, directly to the checking account you pay your rent from.

For $2 a month, Boom will report your rental payment to all three credit bureaus. And for a one-time fee of $25, Boom will report up to 2 years’ worth of past rental payment history to the credit bureaus.

According to Boom, customers who add a rental payment tradeline to their credit reports experience a credit score increase between 10 to 100 points. Here is their own internal data on that:

It is important to note that some of the older credit scoring models, like those used for mortgages, do not include a rental tradeline in credit score calculations.

Experian BOOST™

Experian BOOST™ can add multiple utility payment tradelines to your Experian credit report.

When you sign up, Experian BOOST™ will search through your linked bank account for any recurring payments. This could be for utilities like electric and gas, as well as for services like phone, cable, and even streaming services.

There is no credit check, the service is 100% free, and it will only post positive payment history to the credit bureau. So any missed payments will be left off of your report.

According to Experian, their average customer saw their credit score rise by 13 points.

Conclusion

You may be tempted by the quick credit repair fix offered by companies selling authorized tradelines when you have bad credit. And yes, it can add great tradelines to your credit reports, but the improvements to your credit score could be short-lived.

There are much better tradeline choices for building good credit instead of giving into the shady practice of credit piggybacking.

Opening primary tradelines are better for long-term credit repair even though they may initially lower your score. New credit card accounts can improve credit utilization, while rental payment tradelines can boost your payment history.

Whether you are focused on building business credit or adding personal tradelines to your consumer credit report, having tradelines primarily in your name will help you achieve a good credit score. Also check out our article, How Long Does It Take for Tradelines to Post? to know the timeline on how soon you can start seeing the results from building credit.

And don’t forget, excellent credit isn’t just about new and better tradelines; it encompasses everything that appears on your credit profile. Such as existing tradelines, collections, inquiries, and more. So don’t forget to pay attention to all of the aspects that make up your credit score.

Read the other articles in our tradeline series:

- How Long Do Tradelines Stay on Your Credit?

- Authorized User Tradelines

- How to Get a Free Tradeline

- Types of Tradelines

- Buy Credit Tradelines

- How to Get a Free Tradeline

Amanda Garland is a personal finance blogger living in Dallas, TX. 10 years ago she was living paycheck to paycheck and knew nothing about how credit works. She learned some hard lessons in her fight for financial stability. Now she has a friendly competition going with her husband to see who can reach a credit score of 850 first. She is also a poet, having obtained a Bachelor of Fine Arts degree in Creative Writing.