We recommend products that we love. When you buy through links on our site, we may earn an affiliate commission.

The big finance sites like NerdWallet, WalletHub, and Fit Small Business include big credit cards brands in their “best startup business credit cards with no credit” articles. This is nonsense.

The Chase Ink and American Express cards are not available to small business owners with no personal credit. Approval for those cards requires good personal credit.

So you may be wondering, are there any startup business credit cards with no credit?

Yes. There are more than you may expect. And by the way, none of these are secured credit cards!

The Top 5 Startup Business Cards with No Credit

Comparison of the Best 5 Business Credit Cards with No Credit

| Business Card | Introductory APR | Annual Fee | Foreign Transaction Fees | Rewards |

| BILL Divvy Corporate Card | None | No | No | Up to 7x Points |

| Ramp | 16.74% – 21.74% | No | No | 1.5% Cash Back |

| Capital One Spark Classic for Business | 20.99% | No | No | Unlimited 1% Cash Back on Every Purchase and 5% on Hotels and Rentals Through Capital One |

| Brex | 0% | No | No | Up to 7-8x Rewards, Based on Payments |

1. BILL Divvy Corporate Card

Source: https://www.bill.com/product/spend-and-expense

BILL Spend & Expense (formerly known as Divvy) is an expense management and business budgeting software that also offers businesses a BILL Divvy Corporate Card.

Payment is due in full each month, and they report your payments to Dun & Bradstreet as well as the Small Business Financial Exchange (SBFE) to help build your business credit.

They do not run a credit check to check for eligibility. Their main requirement is that your business has at least $5,000 in expenses each month.

BILL Spend & Expense also offers both digital and physical cards for your employees. You can receive notifications in real-time, track expense reports, and freeze cards when needed.

One of the best perks about the BILL Divvy Corporate Card that you can set budgets and never go over budget again. Everything is recorded and you can review spend over any month that you have used the card, it will even provide a projection of what future budgets could look like.

Your tax consultant will thank you when they see all of your expenses and receipts in one place.

If your employees ever need to purchase something out of pocket, they can also use the app to submit a mobile receipt upload. The budget owners can then approve or deny the transaction through the app and start the ACH direct transfer to your employee’s account. It’s that easy!

It also offers several key perks, including:

- No annual fees

- No foreign transaction fees

- Flexible underwriting and rewards

- Individual employee cards with enforceable budgets

- Integration into their expense management software

Source: https://www.bill.com/product/credit

The BILL Divvy Corporate Card rewards are also top-notch. You can manage them based on your payoff schedule; weekly, semi-monthly, or monthly.

For example, if you select the weekly option, you can receive up to 7x rewards on restaurants, 5x on hotels, 2x on recurring software subscriptions, and 1.5x on everything else.

Overall, your rewards are based on how frequently you make payments.

And if you’re looking for a built-in platform to help manage your business expenses, it’s ideal.

Not only does this help you establish better spending habits, it saves a lot of time with data entry and always gives you a bird’s-eye view of financials.

BILL Spend & Expense also has next-level security where they provide top-performance account security, fraud protection, PCI DSS certification, and SOC2 Type 1 compliance.

The best part is that their spend management software is completely free. There are no hidden fees or contracts. They get paid by the merchants every time you spend money using their card.

Also check out our BILL Divvy Corporate Card Reviews for more information on this card.

2. Ramp

Source: https://ramp.com/corporate-cards

Ramp is based on monthly spending where credit limits are determined by how much you spend.

It also features innovative software that allows you to streamline your finances and manage credit utilization.

Here are the key highlights of a Ramp business credit card.

First, there are no fees involved with an account opening. There’s nothing required for initial setup, no annual fees, no foreign transaction fees, no replacements fees, or anything else, which is perfect if you’re a new small business owner just getting your feet wet.

Next, there’s a simple, straightforward card membership rewards system where you get 1.5% cash back rather than dealing with cocardmplex points.

And because Ramp runs on Visa, it’s accepted by literally millions of retailers and has the built-in security features you would expect from an industry leader like Visa.

It also integrates with Apple Wallet and Google Pay, which is a nice plus and makes purchasing more convenient

In terms of interesting features, there are three, in particular, that stick out.

One is that Ramp gives you maximum control of your business credit so you can block or restrict certain vendors if needed, either on individual employee cards or for your company as a whole.

Source: https://ramp.com/corporate-cards

Another is the ability to “fine-tune each card’s limits by amount, time, or category” so you can fully customize your spending and stay within budget.

Finally, Ramp makes it super easy to manage your cards from a single dashboard, so you know what’s happening in real-time and can make changes when necessary.

Source: https://ramp.com/corporate-cards

3. Capital One Spark Classic for Business

Source: https://www.capitalone.com/small-business/credit-cards/spark-classic/

Of all the startup business credit cards with no credit, Capital One Spark Classic is perhaps the simplest.

There’s a straightforward payment structure where you “pay the greater of $15 or 1% of your balance plus new interest, late payment fees, and any past due amount.”

You get 1% unlimited rewards on every purchase and 5% cash back on hotels and rental cars that you book through Capital One Travel.

And there are no annual fees or foreign transaction fees.

The application process is quick and painless, takes about 10 minutes, and you’ll instantly know whether you’re approved or not.

As for features and benefits, this Capital One small business credit card:

- Has an automatic payments option so you know for sure payments are made on time without having to do it manually (this is huge for protecting your credit score)

- Allows account managers to easily monitor transactions

- Offers detailed purchase records that are compatible with Quickbooks, Excel, and other bookkeeping software platforms

- Provides year-end summaries for streamlined tax reporting

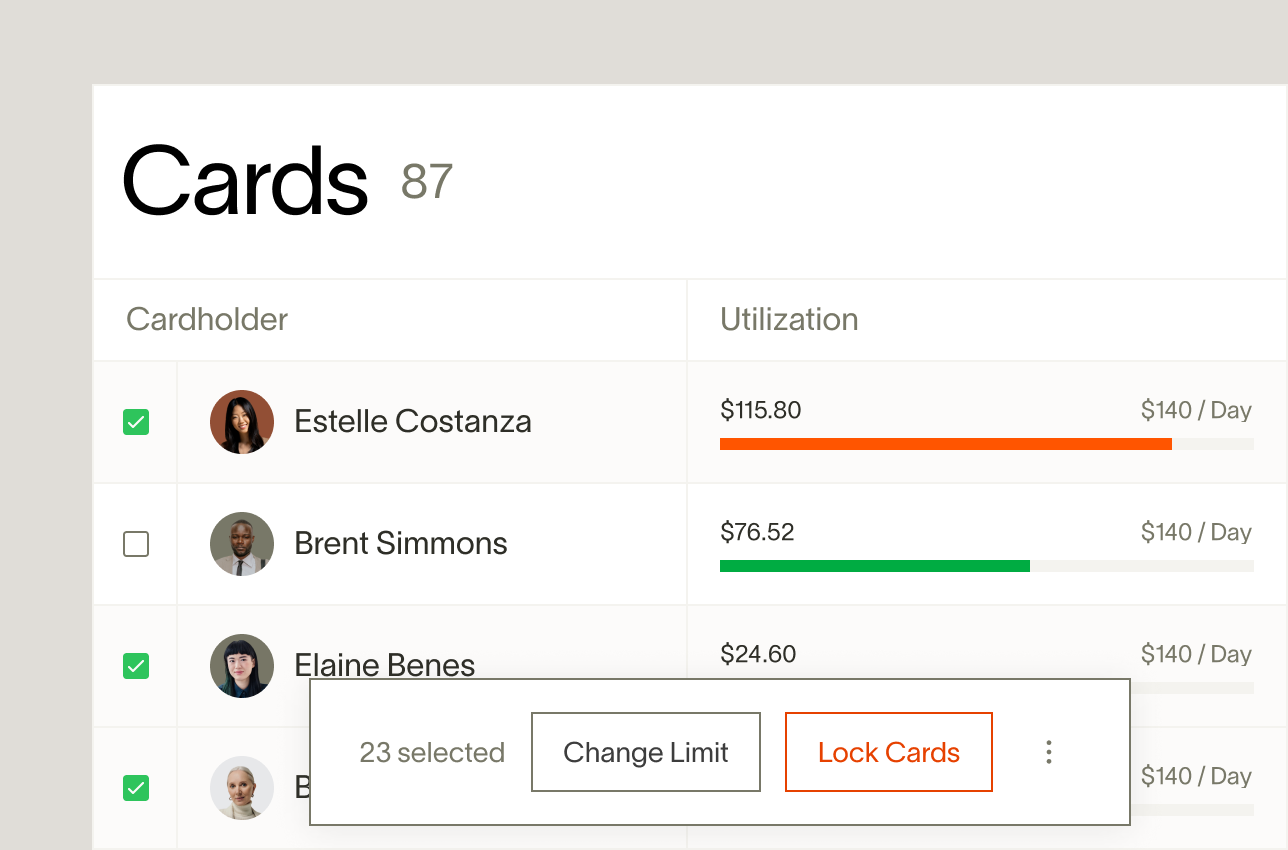

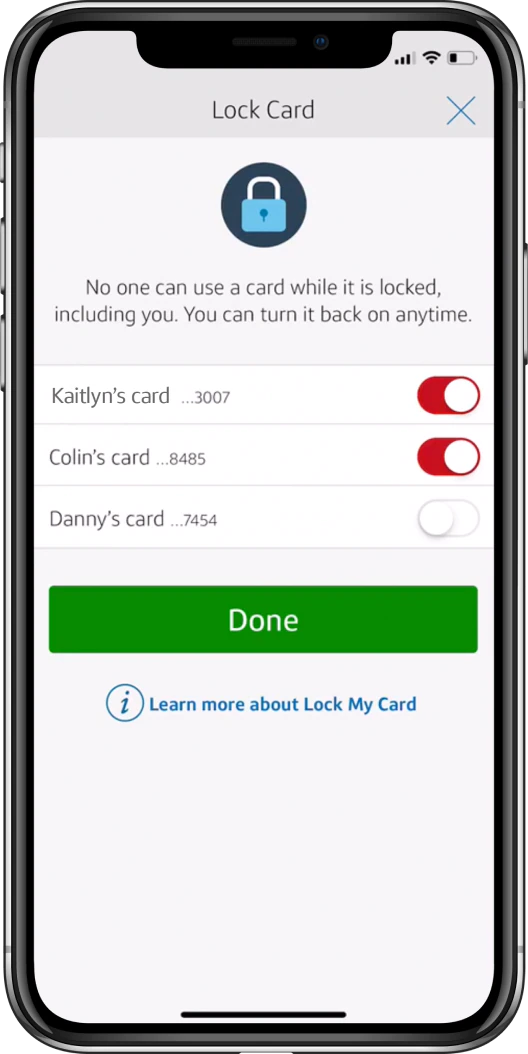

There’s also top-notch security with fraud and security alerts whenever there’s suspicious activity.

And you can lock employee cards or your card if there’s ever an issue like a card being lost or stolen.

Source: https://www.capitalone.com/small-business/credit-cards/benefits/

While there are other small business credit cards with beefier membership rewards, this is a great choice if you have no business credit and are looking to build it by spending responsibly.

The good news is that Capital One is known for catering to customers with “fair credit”. A personal credit score in the low or mid 600s will probably qualify you for this card (assuming that you meet their other criteria.)

But just to be clear, you can’t have no personal credit to get this card. You have to have some good things on your credit report.

4. Brex

Source: https://www.brex.com/product/credit-card/

Note: As of 6/17/22, Brex announced that it won’t be serving normal small business customers. They will require startups that use their services to have venture backing. So while it’s technically a good card for “startups”, it’s not a good fit for most small businesses.

If you’re looking for a small business card that’s all about scalability with plenty of rewards and no fees or interest, Brex will definitely grab your attention.

It’s also perfect if you lack a credit history.

After approval, you can start building or rebuilding credit right away, as a Brex card will draw from your balance daily.

Brex offers 10-20 times higher limits than many other small business cards.

And you can always scale up as your business grows over time.

When it comes to Brex cash back rewards, they’re quite robust, including:

- 8x on rideshares like Uber and Lyft

- 5x on travel

- 4x on restaurants

- 3x on eligible Apple products

- 3x on recurring software

- 2x on lab supplies

- 1x on all other eligible purchases

With Brex, you get unlimited employee cards for every team member — all of which can be easily tracked to stay on top of expenses.

There’s comprehensive fraud protection with zero liability.

And as we mentioned earlier, there’s no annual fee, interest, or other fees. Instead, they simply take a small fee from the merchant whenever you make a purchase with your Brex card.

Besides that, there’s no personal guarantee to separate your business credit and personal credit.

Companies of any size can apply, and there’s no minimum balance, which is great if you’re just starting out with your small business venture.

There’s also simplified expense and rewards tracking through an intuitive dashboard.

Source: https://www.brex.com/product/credit-card/

And Brex integrates with major accounting software like Quickbooks and Xero to dramatically streamline bookkeeping. Also check out our side by side comparison of Ramp vs Brex for more details between the two options.

If you lack a credit history and want to boost your credit score, Brex can help you do it.

How Can Startups Build Business Credit?

For starters, you’ll want to establish your business, create a legal name, and get an employer identification number (EIN).

Your EIN is basically the equivalent to a business Social Security number, which allows the government to identify you and is integral to paying your taxes.

These things get the ball rolling initially and allow you to be officially recognized as a business.

Next, you’ll want to partner with vendors that report to credit bureaus — something to ask about when building relationships. (Second Chance Credit Card with No Security Deposit)

And, of course, after choosing vendors, it’s vital that you consistently pay them on time (early is even better), as this will help build your business credit and credit score when they report to credit bureaus.

Not to mention it’s integral to establishing trust and maintaining healthy long-term relationships.

Another key part of the puzzle is getting a business credit card, which brings us to the topic of this discussion.

Just like using personal credit cards is a big part of building personal credit, a business credit card is an excellent way to boost your business credit.

The key to gaining momentum is to 1) maintain a healthy credit utilization ratio, which is typically a maximum of 30% of your total credit limit and 2) pay on time or early.

As these companies report your payments to credit bureaus, your business credit history should improve, and you’ll have access to more cash in time.

Finally, there are also credit builder business loans through companies like CreditStrong which work similarly to traditional installment loans and help you gradually build your business credit over time.

You can find an in-depth review on CreditStrong here and a list of Secured Business Credit Cards That Report to D&B here.

Should Startup Owners Rely on Business Credit?

No, you need good personal credit.

Ideally, you’ll fix your personal credit and build your business credit at the same time.

It may, honestly, feel like a bit of an uphill battle at first when you’re just starting out.

But as you establish your business as an official entity with the government, consistently make payments on time or early, build rapport with vendors, and establish trust in general, you’ll gain traction.

This combined with diligently working toward building/improving your personal credit should help you maintain a positive trajectory in both areas.

And in the long run, this creates a virtuous cycle where having solid personal credit and business credit gives you access to more cash to further fuel business growth.

But the bottom line is that you shouldn’t rely strictly on business credit.

Do Business Credit Cards Check Personal Credit?

Some do, some don’t.

“When you apply for a business credit card, the card issuer may consider both your business’s track record and your personal credit,” Credit Karma explains. “This could include running a hard credit check on your personal credit.”

Taking a quick look at the pre-qualification criteria should let you know whether they check it or not.

If you have less than stellar personal credit and a business credit card does check it, you’ll probably want to look for an alternative, as this will lower your chances of approval.

Also, note that whenever a company runs a hard credit check, it can potentially lower your personal credit score by a few points.

So this is something to keep in mind with an account opening.

How We Came Up with This List

These are all cards that allow you to have fair or bad personal credit AND be a startup, and they will still let you have a card.

There are two main reasons why card companies like these are lenient with their eligibility.

One is because some can give you a smaller credit line initially and let you scale up as you consistently make payments on time.

Ramp and Brex, for example, are all about scalability.

The other reason is that some have higher than average APRs and added fees.

Indigo is a prime example because, although they’re extremely lenient, they have a high APR and numerous fees to offset it.

While there are definitely other business credit cards with better terms and conditions (Chase Ink Business, Chase Business Platinum, and American Express Blue Business are great examples) the ones featured on this list check the boxes for startups that lack personal credit.

And as long as you’re responsible with your spending and always pay on time or early, these credit cards can serve as the perfect springboard for even better business credit vendors.

Closing Thoughts

Trying to launch a new business with no credit can feel a little intimidating, and you simply won’t be eligible with many business credit cards.

But as we’ve discussed here, there are several solid options available that don’t require any credit, and some allow for bad credit and even a previous bankruptcy.

The five startup business credit cards with no credit listed above are all worth checking out, with each having its own unique features and benefits.

It just boils down to your specific situation and what you’re looking for in a card.

And remember, as your small business grows and your credit score improves, more doors will open.

Also Read:

- 5 Secured Business Credit Cards That Report to D&B

- Ramp vs Brex: Which Is Better?

- BILL Divvy Corporate Card Reviews: Is It Right for Your Business?

- Business Credit Cards vs. Personal Credit Cards

- The 8 Best Business Cards with EIN Only

Nick is an author, small business owner, and finance/digital marketing writer. He’s been covering the industry for over a decade and loves exploring topics to help other small businesses succeed. You can connect with him at Nickmannwrites.com.