We recommend products that we love. When you buy through links on our site, we may earn an affiliate commission.

In simple terms, Nav is a financial tech company that helps small businesses get the financing they need. Their official mission is “to reduce the death rate of small businesses.”

To accomplish that goal, Nav gives business owners insight into their various credit scores, helps organize their finances, and directs them to lenders that might be a good fit. In other words, they’re a bit like Credit Karma for your business.

If you’re interested in getting financing for your company or simply gaining a better understanding of your creditworthiness, Nav has something to offer you. This comprehensive Nav review explains how the service works and when it’s worth using.

How Nav Works

First and foremost, Nav is a credit monitoring tool, much like Credit Karma, Credit Sesame, or WalletHub. What distinguishes Nav from the rest is that it includes services for your business credit in addition to your personal credit.

Nav’s fundamental premise is that you need to thoroughly understand both aspects of your credit to effectively target the types of business financing that make sense for your company.

Without that knowledge, you’ll spend time and money applying for types of financing that you have little to no chance of getting. Not only does that waste resources, but it also means you have to wait that much longer to receive the funds you need.

However, tracking down and organizing your various credit reports and scores on your own can be tedious, tiresome, and surprisingly, hard. Nav streamlines the process and keeps all the data you need in one convenient location online.

The service also takes things one step further by analyzing your credit profile and directing you toward lenders and accounts that seem like they’d be a good fit. That includes business and personal loans, credit cards, and even bank accounts.

If you’re interested, you can also connect your bank accounts to your Nav profile so it can function as a basic enterprise resource planning (ERP) solution and assist with your financial management.

Nav’s Credit Reporting Options

Nav has undergone significant changes in their credit reporting options recently. If you visit their website, you won’t see any free options as you did in the past — only the Nav Prime paid version for $49.99 a month.

However, they still have a free option which includes access to limited editions of your business credit reports. Naturally, you won’t receive as many services with a limited Nav account, but it’s still intact.

Here’s what you need to know about the two credit reporting options.

The Free Version

If you visit Nav’s pricing page, you’ll quickly notice that their free plan has significantly less to offer than their paid plans. That shouldn’t come as much of a surprise. You get what you pay for, after all.

However, that doesn’t mean the free account doesn’t provide anything of value. You’ll still receive all of the following benefits:

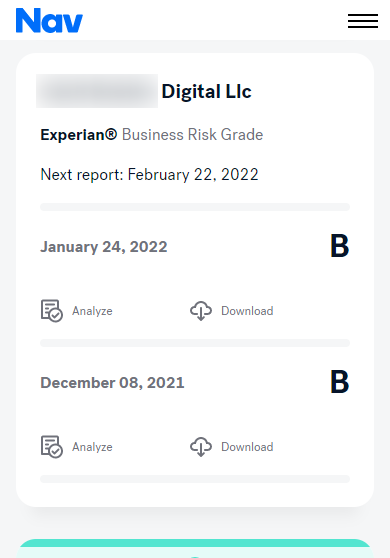

- Summaries of your business credit reports from Dun & Bradstreet, Experian, and Equifax.

- A “business risk grade” that gives you an idea of how good your business credit score is for these three business credit bureaus. (For example, you get a “B” instead of your actual Dun & Bradstreet PAYDEX score of 70.)

- A summary of your personal credit report from Experian.

- Your personal credit score from Experian (VantageScore 3.0).

- Alerts for your business and personal credit profiles.

- Access to their financing marketplace and personalized recommendations for lenders and credit accounts.

- Monitoring and analysis of your business’s cash flows.

- One-on-one access to their credit and lending specialists for recommendations.

The most significant issue is that you don’t get access to the actual copies of your business or personal credit reports with Nav’s free account.

On the personal credit side, you’ll only receive a high-level overview of your accounts, inquiries, and credit history. On the business side, you’ll get something similar, plus a summary of any legal filings or collections impacting your business credit.

You still get a copy of your personal credit score, but only your VantageScore 3.0 using your Experian report. You have to pay to get the TransUnion score.

Unfortunately, you don’t get any of your business credit scores. Instead, they’ll give you a “business risk grade” from A to F. It’s not a legitimate credit score, but it does give you a general impression of your business’s creditworthiness.

If you have a business, we recommend at least getting Nav’s free plan. Business credit information is hard to come by – unlike in personal credit, where you can get that data from any number of places.

Nav is the only “Credit Karma for business” out there. It’s best to know your business credit profile long before you need financing.

What’s even better is that you can track several different business credit profiles on the free plan.

So if there is a big client you’d like to take on, but you’re not sure they pay their bills on time, then you can use Nav to check their credit history for free. This is also valuable for vetting potential business partners.

Or, use it to track your competitors’ business credit. As you can see, this data has a number of great uses.

Nav Prime

Like most tiered subscription services, Nav’s paid option, “Nav Prime”, includes the same perks you get with the free plan and then some and costs $49.99 per month.

It has the following benefits:

- Full access to your business credit reports and scores for D&B, Experian, and Equifax.

- Full access to your personal credit reports and scores for Experian and TransUnion.

- If someone steals your identity, call customer service, and one of their specialists will handle the recovery process.

- Business credit report monitoring for up to five entities.

- The Nav Prime payments gets reported as a tradeline

You can get it for $49.99 per month or $149.97 per quarter.

Nav’s most enticing feature is its credit reporting services. That means they’ll share your membership payments with the commercial credit bureaus as a vendor tradeline, which helps you build your business credit.

It gets reported to D&B, Experian, and Equifax.

If you’re trying to build your business credit, this plan is a super-duper cheap way to do it.

Also, note that business owners who use Nav Prime can increase their business credit scores by up to 50% within the first three months.

It also includes the new Nav Prime Card, which serves as a charge card, and the new checking account.

The Nav Prime Card lets you build credit with everyday purchases and serves as a second monthly tradeline to boost your business credit profile even more. That way, you get two tradelines for the price of one.

Besides that, this card reports to the SBFE in addition to the three main credit bureaus for an even bigger impact.

You can get Nav Prime for $49.99 per month or $149.97 per quarter.

If you’re trying to build your business credit, this option is a super-duper cheap way to do it.

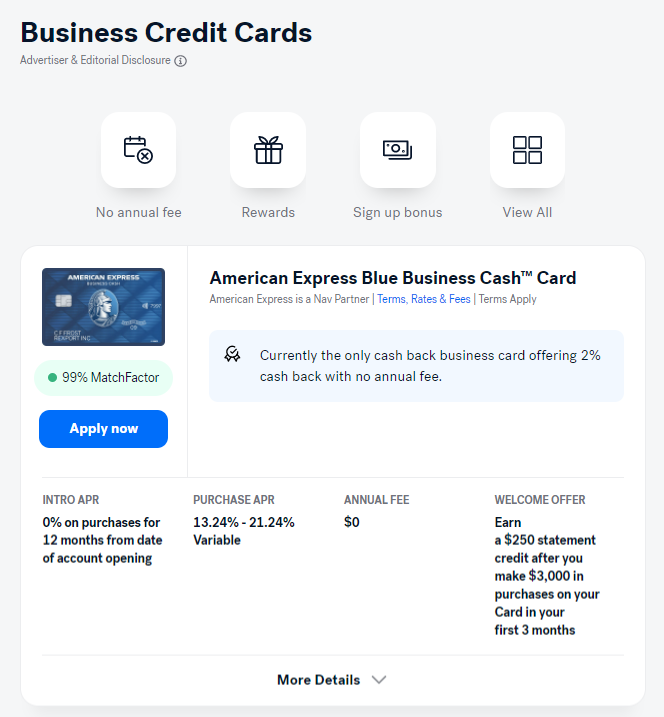

The Business Credit Card Marketplace

Next, let’s take a look at Nav’s credit card marketplace. Using all the credit and financial data that you give them, it’s a tool that points you towards business and personal credit card accounts they think you might be interested in applying for and are likely to get.

The tool provides a detailed summary of the qualification requirements each card issuer considers, such as your personal or business credit score, utilization ratio, and length of credit history. It also indicates how well you stack up against them.

In addition, it consolidates and presents the card’s interest rate and fees, introductory offers, and cashback rewards so you can assess its merits at a glance.

While you can get similar services from many other online providers for your personal credit, no one else offers them for businesses the way Nav does.

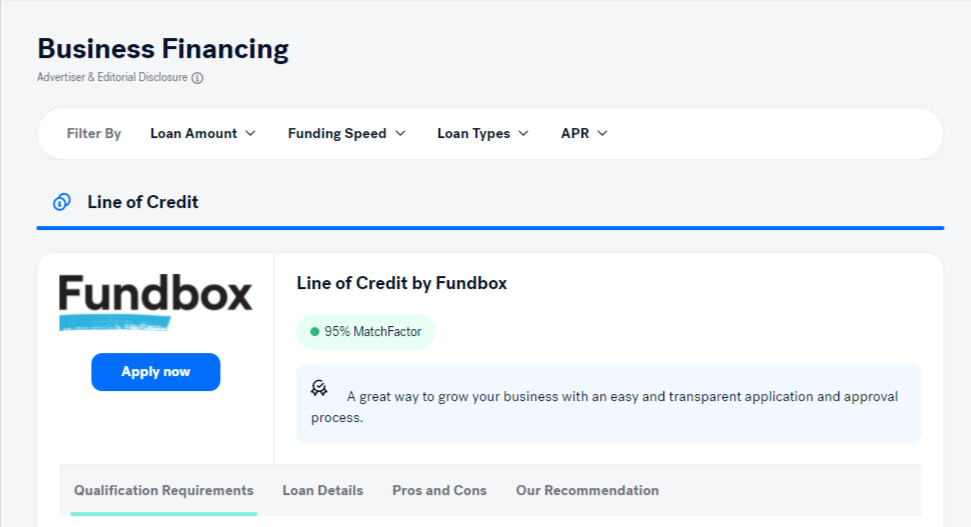

Getting Business Financing Through Nav

If you’re more interested in getting a small business loan, line of credit, or another non-credit card type of financing for your business, Nav has a marketplace tool for that too.

Much like the credit card tool, it uses the information they gather about your personal and business credit profiles, as well as any data you share with them about your finances. They do this to put you in touch with a lender that might suit you.

If they determine your business could qualify for financing from a traditional financial institution like a bank or credit union, they’ll put you in touch with a lender.

However, if you probably won’t qualify for traditional financing because you haven’t been in business long enough, lack the necessary credit scores, or don’t meet minimum annual revenue requirements, they’ll send you to an online lender like OnDeck.

If you have a good relationship with your current bank or credit union, start looking for business funding through them first. If that’s not available, it’s worth considering going through Nav’s marketplace.

Our Verdict

All in all, Nav is a great place for any small business owner interested in credit monitoring or business financing. Fortunately, you can access many of their primary services with a free account.

Because it doesn’t cost you anything, signing up for their lowest-tier account is worthwhile for just about every business owner.

You’ll only get limited insight into your business and personal credit, but you’ll still have full access to their financing marketplace, which automatically recommends products that may be suitable for you.

Nav claims that business owners who get matched to financing options through their site are 3.5 times more likely to receive approval for their business loans and credit cards.

Whether the Nav paid account is worth it depends on your circumstances.

If you’re actively building your business credit, it’s worth it to pay for the full business credit score and report access. The extra vendor tradeline boosts your business credit scores that much faster.

FAQs

Does Nav pull your credit?

Like other credit monitoring services, it uses a “soft pull” to get your credit data. Getting a Nav account (either free or paid) will not put a hard inquiry on your credit.

That means that checking your business or personal credit through Nav will not hurt your credit.

Is Nav an SBA approved lender?

No, Nav is not a lender. However, they can connect you to SBA lenders (at no cost to you) through their matching service.

Keep in mind that SBA loans are hard to qualify for. If your business probably won’t qualify for an SBA loan, they won’t waste your time putting you through the application.

This is where Nav really shines. Rather than apply for a loan and then find out if you qualify, you can basically use Nav’s matching service to see your likelihood of getting approved first.

Is Nav legit for PPP?

Nav was connecting borrowers to PPP program lenders when the program was still in effect. Since the PPP loan program closed, neither Nav’s lender partners nor anyone else are lending on PPP program terms.

Also Read:

- How To Build Business Credit Without Using Personal Credit

- Net 60 Vendors

- Tier 1 Business Credit Vendors

- Tier 2 Business Credit Vendors

- Business Credit Builder

- Credit Strong Business Credit Reviews

Nick Gallo is a Certified Public Accountant and content marketer for the financial industry. He has been an auditor of international companies and a tax strategist for real estate investors. He now writes articles on personal and corporate finance, accounting and tax matters, and entrepreneurship.