We recommend products that we love. When you buy through links on our site, we may earn an affiliate commission.

Fixing your credit on your own is a big undertaking. It can quickly become an overwhelming process when considering all of the dispute letters, correspondence, and tracking. The more complex your credit situation is, the more time you’ll have to dedicate to fixing it.

Many people confuse the terms “credit repair” with “credit building”. It’s an easy mistake to make. Credit repair is the process of getting rid of negative items on your credit report. On the flip side, building credit is when you start adding positive things to your credit history.

If you have bad credit, you’ll have to start with credit repair before you move on to building credit. This is a step-by-step credit repair guide. We’ll show you how to get the negative items off of your credit report. The legal way.

9 Steps of DIY Credit Repair

When you decide to do it yourself instead of hiring a credit repair company, you’d be surprised at what you can do. By following these nine steps to credit repair, you’ll have a handy guide to refer to for each point in your process.

Step 1: Get Your Credit Reports & Review Them

Before you find out what needs to come off your credit reports, you’ll need to know what’s on them first. Many companies, including some credit bureaus, charge a fee to view your credit report and credit score. But it’s not the only way to get your report.

There are free credit report options like Credit Karma, which give you a VantageScore 3.0 credit score. They also provide a detailed view of your credit report. This covers all of the credit cards, student loans, car loans, mortgages, and other credit accounts you may have opened.

Once you have your credit report, you’ll want to take the time to review the information on it. It might be helpful to make a list of your current accounts, credit card balances, interest rates, and credit limits.

Then you will match your list up with what’s on your credit report. This helps you stay organized.

As you look over your credit reports, you’ll want to keep an eye out for any blemishes on your credit history, such as:

- Personal information errors (Wrong address, name typos, etc.)

- Debt in collections or public record accounts

- Accounts with the wrong status listed

- Accounts you aren’t familiar with

- Maxed out credit cards

- Late payments

All of these contribute to a lower credit score. Make note of each one to develop an action plan on what to tackle first. If you like the sound of this, also check out our Dovly Review, which is another option for building credit.

Step 2: Find Errors In Your Credit Report

When you review your credit, you’re not just looking for small typos. You’re also looking for potential errors that could bring down your score and cost you extra money in interest. Oddly enough, that happens more often than you’d think.

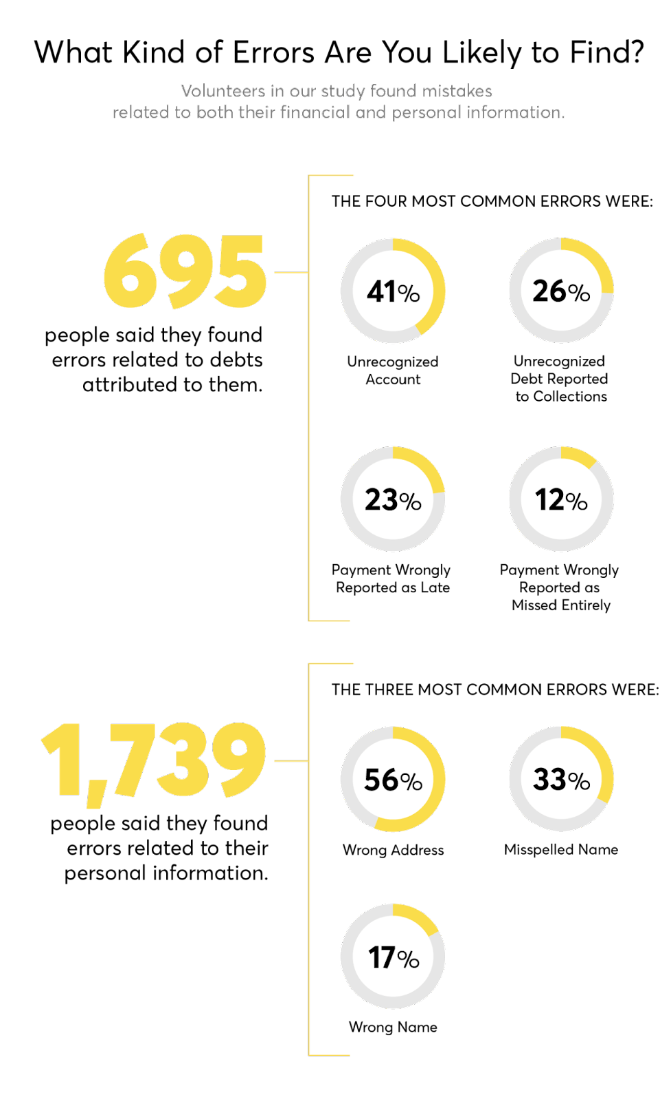

A 2021 study from Consumer Reports uncovered that one-third of about 6,000 volunteers found at least one error on their credit report. These errors ranged from personal information errors to unrecognized debt reported to collections. That causes major damage to your credit.

The same study also noted that 10% of volunteers found it difficult or very difficult to get access to their credit reports. As we mentioned earlier, some credit reporting agencies require a credit card to be supplied for access to your credit report.

Many people are even caught off guard when they find their credit card details are used for a subscription to credit monitoring services that cost up to $30 a month. This makes it costly to take the steps needed to uncover and dispute potential errors.

If you know how to access your free credit reports, you get to skip the hassle and still find what’s holding your credit score back. When you do, here are the biggest issues you’ll want to look for:

- Wrongly recorded late payments

- Accounts you’re unfamiliar with

- Payments falsely recorded as missed

- The wrong name

- Debts reported to collections that you don’t recognize

Errors like showing the wrong name or finding unfamiliar accounts could be a sign of identity theft. Errors involving debt can quickly drop your credit score by up to 100 points.

This makes the process of applying for credit far more difficult and much more expensive than it should be without the mistake. If you’re located in Texas and would like to work with someone more local, check out our Credit Repair Companies in Las Vegas article fore more information.

Step 3: Dispute The Old Addresses and Incorrect Name Variations On Your Credit Report

Start with the easy stuff. Disputing name misspellings or previous addresses is a relatively quick win. It’s easily confirmed and gives you a feel for how the credit repair process goes. It also makes the rest of your disputing process more effective.

To do this, you’ll want to make sure only one correctly spelled name is listed on your credit report. Only your current address should be listed as well.

When you send in your dispute letter to the credit bureaus, you’ll have to include an updated copy of your driver’s license, rental agreement, or mortgage statement as proof of your identity. This is key because it’s proof that the disputed information is incorrect.

Once the credit bureaus receive your dispute request for those incorrect items, they have to complete their investigations within 30-45 days of receiving your dispute.

The response you get back has one of two outcomes:

- The corrections will be made.

- The request was declined.

If your request for a correction was granted, you’ll have to check back in on your credit reports to ensure the changes were made. If the request was declined, you can always appeal it.

If you’re successful, the right name and address should be displayed on your credit report when the credit bureaus update your file. Not only does this make stealing your identity more difficult, but it also makes the potential for confusing your identity with someone else much harder.

Getting your name, address, and other personal information correct first will make your later disputes more successful. So don’t skip this step!

Step 4: Dispute The Other Errors With The Credit Bureaus

Now, you hopefully have a feel for the process by correcting your name and address. Here comes the challenging part – disputing the other errors shown on your credit report. We mentioned some of these earlier, such as falsely recorded late payments or unfamiliar accounts.

Here are some other credit report mistakes that show up pretty often:

- Accounts you’ve closed still showing as open

- Being recorded as the owner when you’re just an authorized user

- The same account was listed multiple times

- Credit card accounts with the wrong credit limit

- Accounts with the wrong balance information

The study that we mentioned before found these errors to be the most common:

While these might not seem as urgent as a fraudulent collections account, these still hurt your credit score. If one of these errors shows on your credit, you should dispute it.

In fact, the Federal Trade Commission (FTC) still suggests doing disputes by mail. It allows you to keep a paper trail and include hard copies of important evidence. Just be sure to send your dispute letter via certified mail to confirm when the credit bureaus received them.

Disputing these errors online might seem like the easiest way to do things, but snail mail might be a better choice in this situation. The Consumer Financial Protection Bureau (CFPB) provides sample dispute letters to use for each credit reporting agency.

Step 5: Wait 30-45 Days for The Bureaus To Respond

Watch paint dry. Catch up on chores. Or get back to the fun things you did before starting your DIY credit repair journey. Sometimes waiting is the hardest part, but it doesn’t take long for you to get an answer.

The credit reporting agencies have 30-45 days to investigate your claim and crosscheck records from the creditors who reported the negative information. In some cases, the creditor may not respond in time or can’t verify the accuracy of what they reported.

That’s when some credit reporting agencies choose to remove the negative information from your credit report. That’s a win! They might also choose to approve your dispute if the evidence you provided along with your letter proves to be a clear error in the information on your report.

Unfortunately, they’re not all winners. Sometimes, even with a good argument and evidence, you might get a decline back from the credit bureau. That doesn’t mean it’s the end of the line for your dispute though. You still have a few options:

- File a new dispute with new evidence for your claim.

- Dispute the negative information directly with the creditor or furnisher.

- Submit a consumer statement as part of your credit report.

- Take it to the next level. Submit a complaint with the CFPB, or hire an attorney.

No matter what the results of their investigation are, each major credit bureau you sent a dispute to must send you the results of their investigation in writing. A little-known bonus of getting your dispute approved is that the credit bureau will send you a free credit report.

Step 6: Submit Goodwill Letters to Creditors For Late Payments

Unless you’re some kind of credit saint, you’ve probably had a situation or five (we’re not judging) where you didn’t have the money to pay the bill on time. It then resulted in a late payment and a serious ding on your credit score.

A goodwill letter explains a financial hardship or other change in finances that caused you to be late on payments. In the letter, you’re asking for the derogatory entry to be removed from your credit report.

They work best for 30, 60, and 90 day late payments. They’re not a guaranteed method for fixing bad credit, but it’s worth a try.

The best goodwill letters have specific goals in mind:

- Explaining why the payments were late

- Asking for the derogatories to be removed and why

- Demonstrating responsibility with a better payment record

Since the late payments are still accurate information, a dispute does no good here. So the derogatory marks stay on your credit report for seven years if you don’t take action.

If you don’t hear anything after sending off your goodwill letter, make sure to follow up with the lender. You can do this by phone, by another letter, or by email. Either way, many people tend to see results with these when they’re persistent about following up.

Step 7: Negotiate Pay-For-Delete For Collection Accounts And Charge-Offs

Although the newest credit scoring models, like FICO Score 9 and VantageScore 3.0, don’t take paid collections accounts into consideration, this is still a viable tactic to raise your credit score if you notice a collection account dragging down your credit rating.

This practice involves negotiating with the collection agency to partially or fully pay off your debt with them in exchange for them deleting the negative information from your credit. This one has a couple of downsides to it:

- There’s no legal backing to a pay-for-delete letter

- It’s technically discouraged by the FCRA

So why try to do it?

Well, most mortgage lenders still use the FICO Score 8 which still counts collections accounts against you. If you want a mortgage but still have accounts in collections, this will help. A lot. Just use caution.

Step 8: Wait Out Public Records… It’s Less Time Than You Think

One negative item on your credit report could be standing between you and a significantly better credit score. But if there’s something serious on your credit report that you can’t remove, you can wait it out.

According to the Fair Credit Reporting Act, a negative entry only stays on your credit report for seven years. If your account was charged off a few years ago, it might be best to wait it out. Especially if you don’t have any pressing needs for new credit.

Serious public records, like bankruptcies, foreclosures, and evictions, stay on your credit report for a long time. However, it’s a common misconception that you have to wait seven to ten years after filing to have a good credit score.

Just because you have a bankruptcy on your history doesn’t mean you have to have bad credit. Even with a bankruptcy on your credit report, it typically just hurts your score for the first two years. It’s possible to get 720+ credit scores within two years of filing bankruptcy.

This is worth repeating: most bad items on your credit report don’t hurt your credit scores very much after two years. So if you work on building your credit in the meantime, your credit scores can bounce back in just two short years. Not seven!

Step 9: Build Your Credit While You’re Waiting

Believe it or nor, it is possible to get an 800 credit score after a bankruptcy, check out our article, How to Get an 800 Credit Score After Bankruptcy, for more information on it.

After you’ve done all the work to erase the negative information from your credit report without the help of a professional credit repair company or credit repair software, you should pat yourself on the back. Then you’re going to start the work of building your credit.

For people with poor credit, this looks like opening a secured credit card. A small security deposit gets you a new credit line to help demonstrate responsibility with revolving credit. These are the best credit cards for people who struggle to qualify for traditional credit cards.

This might also include:

- Improving your credit utilization ratio by paying down credit card debt

- Using credit counseling services to come up with a debt repayment plan

- Building credit with new tradelines

One of the best things you can do to build your credit is to use one of the approved Digital Honey vendors to open a new tradeline. As long as you’re making on-time payments, you’ll see improvements in your credit score.

FAQs

What Is the Fastest Way to Repair Your Credit?

Credit repair isn’t a fast process. Even a credit repair company or credit pro will require three months to a year or more to reach a good credit score if you started with bad credit.

Many people have more success and faster results when they DIY their credit repair. Because who knows your credit better than you do?

How Can I Fix My Credit With No Money?

DIY credit repair is the best way to fix your credit if you’re short on cash. You can easily pull a free credit report and get free resources from government agencies like the CFPB and FTC to help you through the process.

What Is a 609 Dispute Letter?

A 609 dispute letter is a theory based on section 609 of the Fair Credit Reporting Act. However, that section of the act isn’t written to aid in the dispute process. It just allows you to request copies of your credit reports and relevant information.

The thought behind it is if the credit bureau can’t supply copies of the original contracts or negotiable instruments, then the negative item is considered unverifiable and has to be erased. This isn’t true. There are no 609 dispute letters that act as a magic eraser for your credit report.

Dispute letters work – but naming section 609 doesn’t make them more effective.

- Why did my credit score drop for no reason?

- Sample Letter to Remove Closed Accounts From Credit Report

- Is 670 a Good Credit Score?

- How to Increase Your Credit Score to 800

- The Best Way to Check Your Credit Score

Seychelle is a Maryland-based personal finance writer and business owner. She’s passionate about helping others out of financial pitfalls she’s already dug herself out of. Most of her finance knowledge stems from her career as a Financial Consultant and Branch Manager at the 7th largest US bank. Read more of her work on credit, budgeting, debt consolidation, and entrepreneurship at www.seychellewrites.com