We recommend products that we love. When you buy through links on our site, we may earn an affiliate commission.

A second chance credit card is designed specifically for people with bad credit. And, fortunately, there are several options available, with some not even requiring a security deposit.

Here are our top five picks, including key details like introductory APR, annual fees, rewards, and more, along with answers to frequently asked questions.

The Best 6 Second Chance Credit Cards with No Security Deposit Compared

| Credit Card | Introductory APR | Annual Fee | Foreign Transaction Fees | Rewards |

| Mission Lane | 19.49%-29.99% | $0-$75 | 3% | Unlimited 1%-1.5% Cash Back |

| Petal 1 | 22.24% – 31.74% | No | No | 2% – 10% Cash Back |

| Grow Credit | 0% | Varies by Plan | No | None |

| Self Visa Card | 26.24% | $25 | No | None |

| Tomo | 0% | No | No | 1% Cash Back |

Mission Lane

The main purpose of Mission Lane is to give people with poor credit an opportunity to get back on their feet.

They really do want to work with people looking to improve their credit. Their non-rewards card accepts people with credit scores of at least 525 – that’s low!

To accomplish this, they give you access to your credit score at all times, equip you with credit-building education tools, and report to the three major credit bureaus.

Mission Lane also gives you the chance to raise your credit limit over time as you prove your trustworthiness by using your card responsibly and consistently making payments on time.

So if you’re looking for a second chance credit card with plenty of forgiveness, Mission Lane is right up your alley.

When it comes to APR, they currently offer 19.49% – 29.99%. If it’s on the low end, that’s pretty reasonable for a second chance credit card.

If, however, it’s on the high end closer to 29.99%, that can be a little steep, and you’ll want to be diligent about making payments on time to avoid excessive interest.

As for the annual fee, it ranges from $0 – $75, and you’ll earn unlimited 1% – 1.5% cash back with Mission Lane, which is solid given it’s a second chance credit card with no security deposit.

You can get a full rundown of cardholder terms and conditions here.

Petal 1

Petal 1 from Visa has a very forgiving philosophy, making it ideal for people with bad credit but who are ready to get back on track.

In their own words, “Credit scores don’t tell the whole story. Petal 1 can look beyond your credit score to create a Cash Score based on your banking history. Your Cash Score shows your creditworthiness and can help you qualify for more credit at better rates.”

So even with a long history of bad credit, Petal 1 can be the perfect credit card issuer to help you turn the corner.

And there are some serious advantages of using Petal 1.

For starters, it’s an unsecured credit card, meaning you don’t have to pay a security deposit.

There are no annual fees or foreign transaction fees.

There’s an AutoPay feature that will automatically pay your balance so you never miss a payment and get hit with late fees.

And Petal 1 offers 2% to 10% cash back at many popular merchants, making it one of the better cash rewards credit card options.

Credit Karma even lists them as one of their favorite second chance credit cards.

While the credit line is limited to $300 to $5,000 initially, this can be increased after six months through Petal’s Leap program as long as you consistently make payments on time and maintain a solid credit score.

Also, you can connect your Petal credit card to Apple Pay or Google Pay (no Cash App at the moment) for added convenience when making purchases.

When it comes to introductory APR, it ranges between 22.24% and 31.74%.

While that’s admittedly high, especially as you approach 30% or more (the current US average is 20.82%), Petal 1 can be a great unsecured card for many people when used responsibly and can help build credit.

Grow Credit

This is one of the more unique credit cards, as it’s designed specifically for paying subscriptions like Spotify, Netflix, and Hulu.

While it’s probably not viable if you need a serious credit line (the basic membership plan has just a $17 monthly spending limit), it can work if your main goal is to build good credit.

With Grow Credit reporting to the major credit bureaus, you can use it as a credit builder to quickly improve your credit score and get into a better financial situation.

And if you already use subscription-based services like we just mentioned, you can set up automatic payments to gain momentum with basically zero effort.

Here are the key details.

Grow Credit has four types of plans.

The Build plan is completely free to use but only has a $17 monthly spending limit ($204 annually). For those who don’t meet the Build underwriting criteria, however, the plan costs $1.99 per month.

The Grow Membership plan costs $3.99 per month and has a $50 monthly spending limit ($600 annually).

And the Accelerate Membership costs $7.99 per month and has a $150 monthly spending limit ($1,800 annually).

You also need a checking account for identification purposes.

Note that Grow Credit does not charge interest, making it a second chance credit card with no security deposit and 0% APR.

Given how unconventional this unsecured credit card is, we can’t say it’s for everyone, especially if you want a large credit limit.

Also, having monthly membership costs can, admittedly, be a turnoff.

But if you’re looking for a simple way to bolster your credit score (an improvement is usually noticeable within 60 to 90 days), this is certainly an option to consider and can help improve bad credit.

Self Visa Card

Let us be totally transparent about the Self Visa Card.

It’s technically an unsecured credit card that doesn’t require a security deposit. But there’s a caveat.

To be eligible, you must first sign up for a credit builder account with Self.

Then you must reach at least $100 in saving progress and make your last three monthly payments on time without any outstanding fees.

At that point, you choose how much to use as your security deposit, which will set your credit limit.

Self will then send you your credit card, and you’re on your way to tackling bad credit and improving your credit score.

Self Visa Card reports to the three major credit bureaus, and it can be the catalyst for achieving a better credit history.

And as long as you continue to make your payments on time, you may have opportunities to increase your credit limit in the future.

While the process of getting accepted for this credit card is a little convoluted, we still consider it one of the best credit cards without a credit check overall.

As for interest, there’s a 26.24% variable APR. There’s also a $25 annual fee and no rewards.

If you have fair credit, this may not be the best second chance credit card for you.

But if you have bad credit and are looking for an effective way to break the debt cycle, it’s definitely worth considering.

Tomo

Tomo is one of the more innovative second chance credit cards and offers some serious selling points.

For starters, there’s 0% APR and no fees.

Next, they don’t look at your credit score to determine eligibility.

Or as Tomo puts it, “you are worth more than just a number (aka an arbitrary credit score). We evaluate individual circumstances and take into account alternative metrics to determine your credit worthiness.”

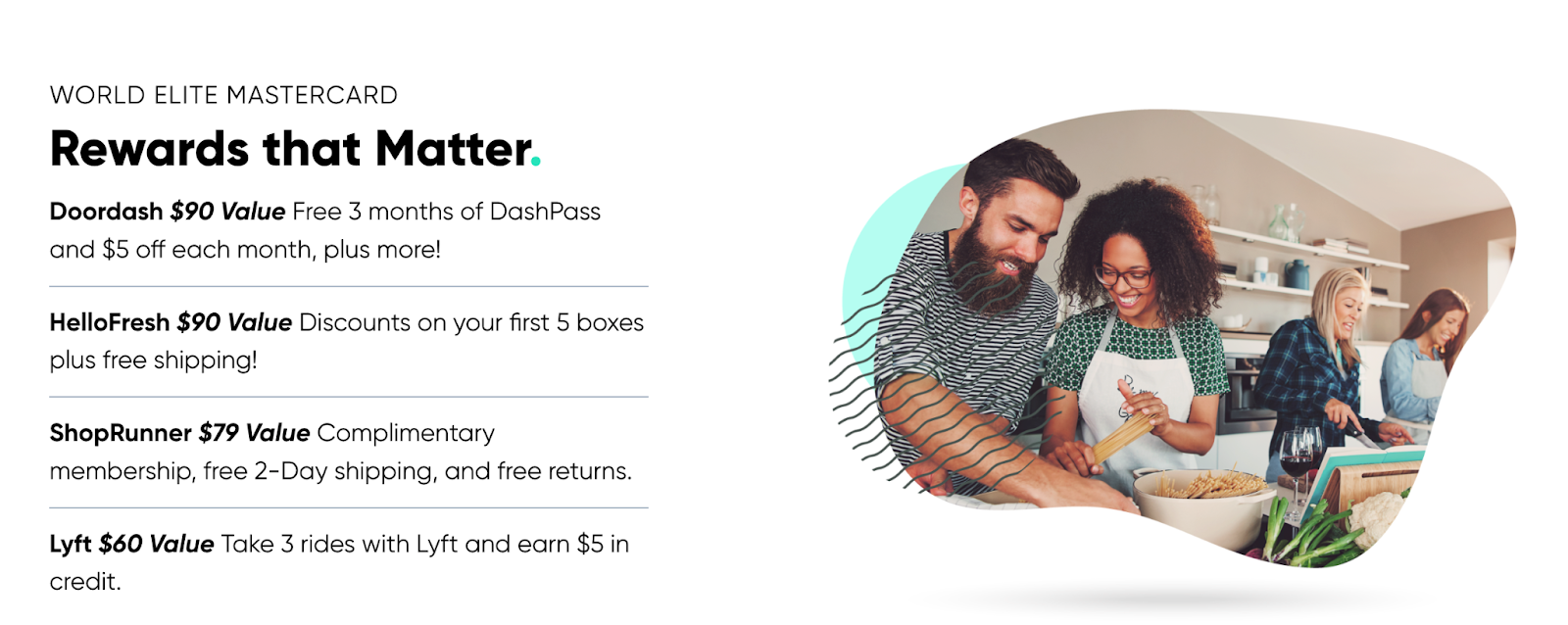

There’s up to $10,000 in spending power, which is light years above many similar second chance credit cards.

They also offer some robust rewards from brands like Doordash, Hello Fresh, Lyft, and more.

While the 1% cash back rewards rate is below average for most credit cards, it’s still solid for a second chance credit card.

And like many of the other credit card providers, they report to all the major credit bureaus, which means you can build credit with Tomo and raise your credit score.

They even offer expedited and automated payment options to get the ball rolling even quicker.

If you’re looking for a highly inclusive second chance credit card with some enticing features, Tomo should definitely be on your radar.

How We Picked These Cards

The main thing we based our choices on was leniency.

Each credit card mentioned is extremely lenient on bad credit and doesn’t perform a credit check.

And as long as you use your card responsibly and consistently make payments on time, it can also help you build credit.

While that often means a higher APR than what you find with traditional credit cards, as is evident with Petal 1, and Self Visa Card, it provides an opportunity for those with bad credit to improve.

The other biggest factor was no security deposit.

While a Self Visa Card does operate like a secured credit card in the sense that it requires you to reach at least $100 in saving progress, it’s technically an unsecured credit card.

And all of the other options serve as a second chance credit card with no security deposit in every sense of the word.

Beyond that, we factored in fees, rewards, and overall user satisfaction.

After crunching the data, these were the top second chance credit cards we came up with.

FAQs

How Can I Get a Credit Card with No Security Deposit?

You just have to find a card issuer that doesn’t include a security deposit as part of their eligibility process.

Fortunately, there are plenty of credit cards that don’t require a security deposit, including many unsecured credit card providers.

All of the credit cards mentioned on this list fall under that category.

What Credit Card Has No Security Deposit?

Petal 1, Grow Credit, and Tomo have no security deposit whatsoever.

The Self Visa Card doesn’t have one either. However, they do require you to reach a minimum of $100 in saving progress before gaining eligibility.

This means that, unlike a secured credit card, you don’t have to put up any collateral to be approved. Instead, a card issuer will look at other factors like individual circumstances.

If you’re curious about finding the best secured credit card, you can get a full overview here.

Will Credit Card Companies Give You a Second Chance?

Yes!

There are several companies that won’t look at your credit history or credit report when determining eligibility.

This makes an unsecured credit card ideal if you have bad credit and want to improve your credit score.

Note that, however, in many cases, this can translate into a higher APR or lower borrowing limits (a secured credit card, by comparison, will tend to have a slightly lower APR).

But it’s definitely possible without a credit check, and many companies will extend their borrowing limits as you prove yourself trustworthy.

It can also serve as a great credit builder account to gain momentum.

Can You Get an Unsecured Credit Card After Bankruptcy?

Yes, it’s possible to get an unsecured credit card after bankruptcy.

However, bankruptcy makes it significantly more difficult to get approved for a credit or debit card and often comes with extra fees and low credit limits.

But if you stay the course and prove yourself to be a trustworthy borrower, you can often move past bad credit.

Note that if you’ve filed for bankruptcy, you may be better off looking at secured cards, as a secured card tends to be easier to obtain.

Also Read:

- Best Credit Card for Contractors (Our Top 6 Choices)

- How to Use a Credit Card to Build Credit

- If I Pay Off My Credit Card in Full, Will My Credit Go Up?

- Choosing Between a Credit or Debit Card for a Teenager Simplified

- The Best Credit Card Alternatives in 2023

- The 10 Best Virtual Credit Cards in 2023

- Credit Cards for Bad Credit [No Deposit Needed]

Nick is an author, small business owner, and finance/digital marketing writer. He’s been covering the industry for over a decade and loves exploring topics to help other small businesses succeed. You can connect with him at Nickmannwrites.com.