We recommend products that we love. When you buy through links on our site, we may earn an affiliate commission.

In 2021, only 30% of small business owners1 were able to secure the financing they needed.

But business credit company, Tillful, is looking to change that with its new secured business credit card.

Here’s everything you need to know about this modern credit platform.

What is Tillful?

Source: Tillful

In its own words, “Tillful’s mission is to unlock capital for the smallest of businesses by using better data.”

It does this in three main ways.

One is by providing small business owners with an accurate business credit score so they’ll know their financial health and can keep track of their report without having to put their personal credit on the line.

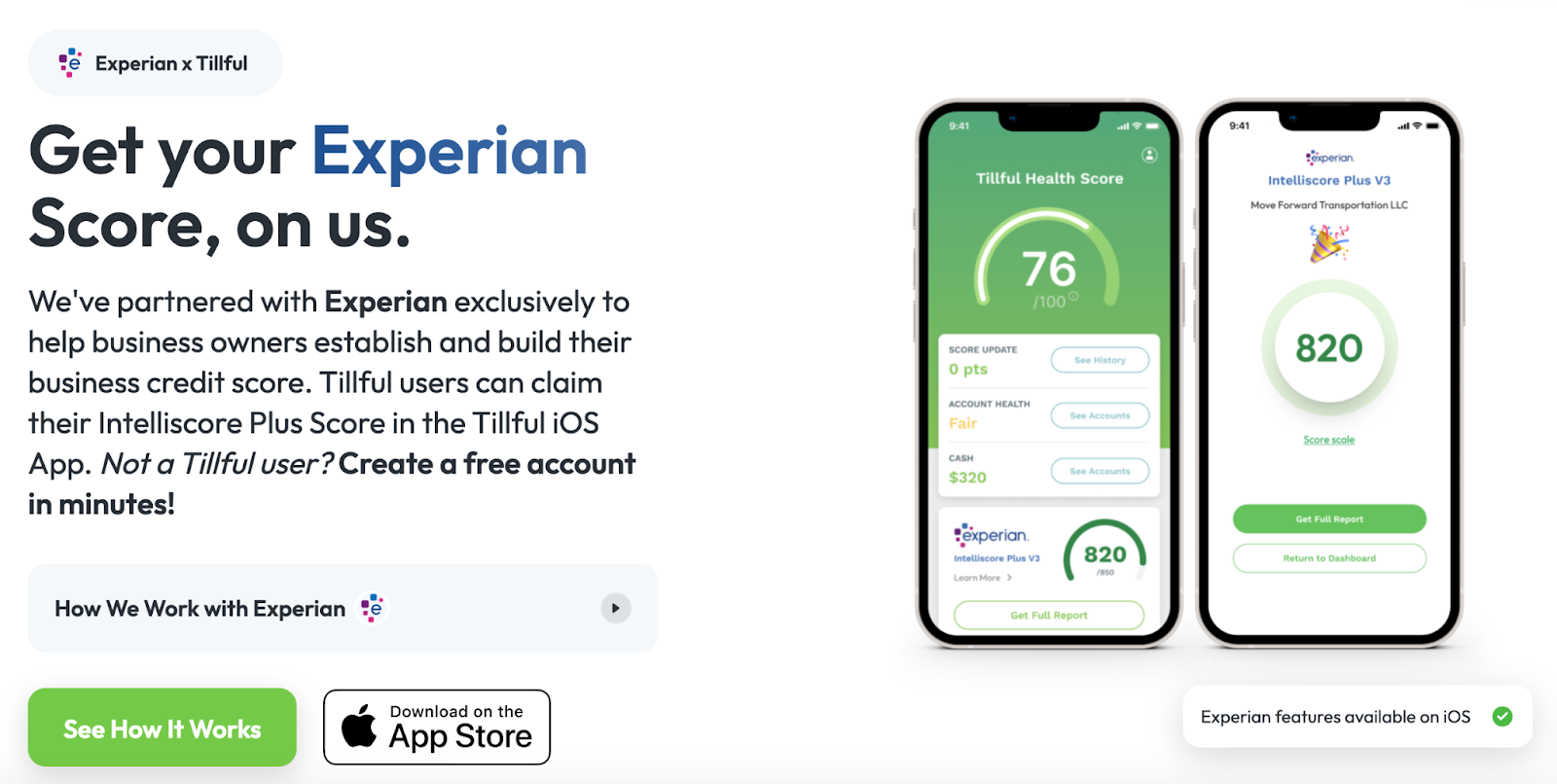

This is done by generating a Tillful business credit score, similar to what Credit Karma does for a personal credit score.

Source: Tillful

It’s also done by generating an Intelliscore Plus Score—Experian’s premier business credit scoring system.

Source: Tillful

Through Tillful’s partnership with Experian, it’s able to provide business owners with an accurate, free business credit score, which is a critical precursor to getting funding.

Another way Tillful helps is by assisting business owners with the process of applying for funding.

Source: Tillful

Tillful will, for example, help a small business owner determine what they’re eligible for and walk them through the application process, which is ideal for those learning the ropes of business funding.

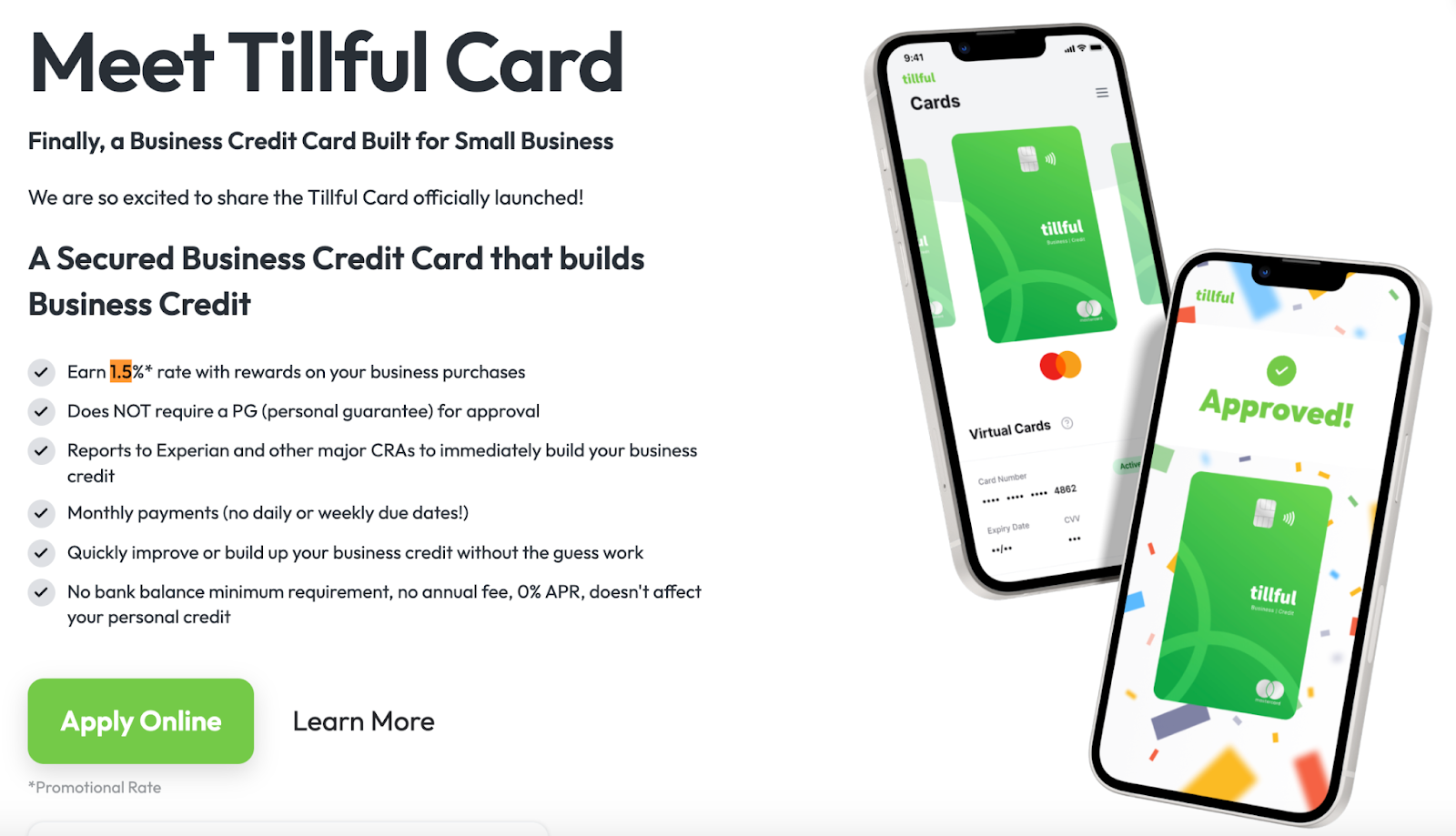

Lastly, Tillful offers a business credit card called the Tillful Card—a new secured business credit card that provides funding while also building business credit.

Plans and Pricing

The Tillful Card has no annual fee or minimum bank balance minimum requirement. However, because it’s a secured business credit card, you’re required to put a deposit down for your credit line.

Source: Tillful

The amount you deposit will determine how much your credit line is.

If, for example, you deposit $1,500, your credit line will be $1,500. Currently, Tillful requires a minimum deposit of $500.

Note that the Tillful Card doesn’t require a personal guarantee for approval and it won’t impact your personal credit score or potentially lead to bad credit.

To qualify for this business credit card, your business must:

- Be incorporated in the US and have a valid EIN

- Be incorporated for at least three months

- Not be in a restricted industry outlined by Sutton Bank

- Have an existing Tillful credit bank account and comply with Tillful’s terms and conditions

Pros

Tillful has a lot going for it and is one of our favorite secured business credit card lenders at the moment.

Here are some specific reasons why we consider them as one of the better lending partners.

Great for Building Business Credit

It’s the only secured-based credit model that reports to the three major busienss credit bureaus AND doesn’t report your personal credit or require a personal guarantee.

More specifically, Tillful reports to Dun & Bradstreet, Experian Business, and Equifax Business.

This is incredibly important if one of your main goals is building business credit to, in turn, achieve a good credit score, qualify for Small Business Administration (SBA) loans, and generally increase your cash flow.

To build your business credit, you want credit accounts that report to the business credit bureaus but not the personal bureaus. If you want to graduate to qualifying for tier 2 business credit vendors, you need starter accounts like Tillful first.

By maintaining a good payment history, your business credit grows. This puts you on your way to improving your credit history, obtaining a good credit score, and potentially receiving other credit offers down the road.

Just be sure to fulfill your financial obligations by making payments on time and maintaining a healthy credit utilization ratio. Once you do this, you’ll quickly be on your way to building business credit. Also check out our list of Best Credit Building Apps if you prefer using apps for building credit.

Solid Credit Card Terms

This is where Tillful wows us.

There’s no annual fee or other fees. You earn a 1.5% rate with rewards on business purchases.

And get this. There’s a 0% APR!

With the average introductory APR of most business cards being over 18% as of mid-2022, you can’t beat it.

And when it comes to making payments, Tillful only requires you to make monthly payments, as opposed to daily or weekly like many other business credit cards.

Free Business Credit Score

As we discussed earlier, Tillful has a partnership with Experian, which is not only one of the business credit bureaus but also one of the three major consumer credit bureaus.

Tillful leverages this relationship to provide users with the Experian Intelliscore Plus Score.

Source: Tillful

As CreditStrong explains, “Intelliscore Plus is Experian’s premier business credit scoring model. To calculate the score, Experian pulls over 800 company and owner datapoints”—thus making it highly comprehensive.

In turn, you can get an accurate, objective snapshot of your business credit score, which is an integral part of understanding business financial health, minimizing your risk level, and improving your credit rating.

You can learn more about CreditStrong in our review.

Cons

Requires a Security Deposit

Again, this is a secured credit card, meaning it requires a cash deposit with the minimum amount being $500.

While most business owners would probably agree that a $500 cash balance is pretty reasonable, it’s not ideal for everyone.

If you’re on a shoestring budget where you’re counting every penny, a secured credit card may not be right for you.

In that case, you would likely be better off getting an unsecured card through lenders like Capital One Spark Cash for Business or Chase Ink Business Unlimited (assuming you’re eligible, of course).

It’s a Brand New Company

The other main issue is that Tillful is still so new.

It was only in October 2020 that the company had its official launch. And the credit card is even newer, launching in June 2022.

Like most new products, it usually takes some trial and error to work out the kinks and get it just right. Therefore, there are likely to be some hiccups along the way. (See also our Startup Business Credit Cards with No Credit article.)

So if you’re turned off by brand new lenders that still need to sort out the details, this may not be the right business credit card for you (at least not at the moment).

Tillful Reviews: Our Verdict

What do we think of it overall? Honestly, it’s great, we love it.

Tillful is a breath of fresh air for business funding and can provide the spark needed to help small business owners obtain financing while also building their business credit.

But since Tillful is a new company, we haven’t had the opportunity to read customer reviews yet. So it’s a bit early to officially give it a full stamp of approval.

That said, Tillful has created quite a buzz recently and has been featured in top publications like Bloomberg and TechCrunch.

If you’re looking for a secured business credit card that will report to a credit bureau with 0% APR, no fees, and other perks like a 1.5% APR rate and enjoy being part of something new, Tillful is definitely worth considering.

If, however, you’re gun-shy about trying out a brand new card, you’ll probably want to hold off until there’s a solid body of objective reviews from users.

Sources

1. https://www.americanbanker.com/news/small-business-owners-struggling-to-get-approved-for-loans-fed#:~:text=Back%20in%202019%2C%20some%2051,and%20just%2030%25%20last%20year.

Also Read:

- Do Business Credit Cards Affect Personal Credit?

- Which Business Credit Cards Do Not Report Personal Credit?

- Is It Illegal to Use a Business Credit Card for Personal Use?

- How Do Business Credit Cards Work?

Nick is an author, small business owner, and finance/digital marketing writer. He’s been covering the industry for over a decade and loves exploring topics to help other small businesses succeed. You can connect with him at Nickmannwrites.com.