We recommend products that we love. When you buy through links on our site, we may earn an affiliate commission.

It’s easy for contractors to run into cash flow issues.

But when used responsibly, the right credit card can keep things flowing as you move from one job to the next, and in some cases, build personal credit.

Here are the best credit cards for contractors based on APR, annual fees, rewards, and more.

The Best Credit Cards for Contractors

- American Express Blue Cash Card

- The Business Platinum Card® from American Express

- Capital One Spark Miles for Business

- Ink Business Unlimited® Credit Card

- Lowe’s Business Rewards Card from American Express

- The Plum Card® from American Express

Best Credit Cards for Contractors Compared

| Credit Card | Introductory APR | Regular APR | Annual Fee | Rewards |

| American Express Blue Cash Card | 0% APR for account opening the first year | Variable 16.24 – 24.24% | None | 2% cash back on each eligible purchase up to $50,000 per year and 1% after that |

| The Business Platinum Card® from American Express | Variable 17.24 – 25.24% | Variable 17.24 – 25.24% | $695 | 5x points on flights and prepaid hotels, 1.5x points on key business purchases and each eligible purchase of $5,000 or more up to $2 million per year, and 1x points on other eligible purchases |

| Capital One Spark Miles for Business | Variable 23.99% | Variable 23.99% | No annual fee the first year and $95 per year after that | 5x points on hotels and rental cars booked through Capital One Travel and 2x on every business purchase |

| Ink Business Unlimited® Credit Card | 0% APR the first year | Variable 15.49 – 21.49% | None | 1.5% unlimited cash back |

| Lowe’s Business Rewards Card from American Express | Variable 18.74 – 27.74% | Variable 18.74 – 27.74% | None | 5% cash back the first six months and 2% cash back after that on eligible purchases at Lowe’s, 2% cash back on business categories, and 1% cash back on all other purchases |

| The Plum Card® from American Express | N/A | N/A | $250 | Unlimited 1.5% cash back on the balance you pay within 10 days of the due date |

American Express Blue Cash Card

Source: American Express

There are four main things we love about the American Express Blue Cash Card.

First, it has some of the most simple rewards terms of all the credit cards on this list.

You earn 2% cash back on eligible purchases per year for up to $50,000. Then you earn 1% cash back after that.

If you hate scratching your head at complex rewards and just want something straightforward that applies to most contractor purchases, Blue Business Cash is right up your alley.

Second, there’s a 0% APR the first year, which makes it great for contractors that are just getting established and don’t want to drown in interest.

And with a variable 16.24 – 24.24% APR after that, it’s still fairly reasonable.

Third, there’s no annual fee with this small business credit card, which is always a plus. And the balance transfer fee is only $5 or 3% of the balance transfer, whichever is greater.

Finally, American Express Blue Business Cash offers flexible buying power so you have access to more cash flow when you need it.

“Expanded Buying Power gives you the flexibility to exceed your credit limit while earning Membership Rewards® points or cash back on your purchases. It can give you more cash on hand for unexpected surprises or big business opportunities.”

As long as you use Blue Business Cash responsibly, you should be able to get more money, which can come in handy with all the unknowns of being a contractor (e.g. slow-paying clients and delays).

Put this all together, and we rank the Blue Cash Card as the best credit card for small business contractors overall.

The Business Platinum Card® from American Express

Source: American Express

Let’s start by addressing the elephant in the room.

The Business Platinum Card® from American Express has a hefty $695 annual fee, making it the highest on this list by a large margin.

So if you’re not into big annual fees, this probably isn’t the best business credit card for you.

The variable 17.24 – 25.24% APR is okay, but not great.

That said, the Business Platinum Card® does boast some impressive rewards similar to Chase Ultimate Rewards.

And that’s the main selling point of this credit card.

With it, you get:

- 5x points on flights and prepaid hotels booked through American Express (just like Ultimate Rewards)

- 1.5x points on eligible purchases in key business categories, such as construction suppliers and electronic suppliers

- 1.5x points on eligible purchases of $5,000 up to $2 million per year

- 1x points on all other eligible purchases and combined purchases

Source: American Express

Besides that, you can earn 120,000 reward points if you spend $15,000 on qualifying purchases within three months of getting your card.

For that reason, the $695 annual fee can be worth it if you plan on spending a lot and want massive rewards that can easily be redeemed for gift cards.

And if you’re a frequent traveler moving from different job sites, the 5x travel points can make it even more enticing.

Capital One Spark Miles for Business

Source: Capital One

Another membership reward program that caters to frequent travelers is the Capital One Spark Miles for Business.

Like Spark Cash Plus, it offers unlimited 2x miles for every purchase and 5x on hotels and rental cars that you book through Capital One Travel.

And if you spend $4,500 within the first three months, you get a 50,000 miles bonus with this card.

Capital One Spark Miles also offers a $100 credit for Global Entry or TSA PreCheck.

So if you’re a frequent traveler, you can rack up some serious points in a hurry that you can funnel back into your business.

Source: Capital One

If, for example, you spent $10,000 a month with your Capital One Spark Miles card, you could earn 240,000 miles rewards a year.

As for negatives, the variable 23.99% APR is higher than other Capital One cards like the Capital One Spark Cash 1.5% Select, which is between 16.24 – 22.24%.

That’s why it’s important to use this card responsibly and consistently make payments on time.

And while there’s no fee for an account opening and no annual fee for the first year, you do have to pay $95 per year after that, which isn’t ideal compared to other business credit card options like Capital One Spark Cash 1.5% Select with no annual fee.

But when you look at the big picture, Capital One Spark Miles for Business can be a great choice for contractors that do a lot of traveling and want a lot of bang for their buck with a travel rewards credit card.

Ink Business Unlimited® Credit Card

Source: Chase Credit Cards

The Ink Business Unlimited® Credit Card from Chase has a lot of similarities to the American Express Blue Cash Card.

There’s 0% APR the first year, no annual fee, and a straightforward rewards program.

One difference is that the Ink Business Unlimited card has a lower APR (15.49 – 21.49% compared to the Blue Cash Card at 16.24 – 24.24%.

It also has slightly less cash back (1.5% unlimited cash back compared to the Blue Cash Card offering 2% cash back on eligible purchases up to $50,000 per year and 1% after).

While you won’t get quite as much cash back on some purchases, the Ink Business Unlimited card offers cash back on everything (not just eligible purchases) and extends beyond $50,000 a year like the Blue Cash Card.

And with one of the lower APRs among the business credit cards on this list, this is a popular choice for many contractors.

Also, note that you get a $750 cash back bonus if you spend $7,500 within the first three months of an account opening, and you can easily get an employee card at no additional cost.

Although it doesn’t have the flashiness of some other cards with robust rewards programs, we still think it’s solid.

When you combine that with a low APR, no annual fee, and 0% APR the first year, it’s an all-around great card.

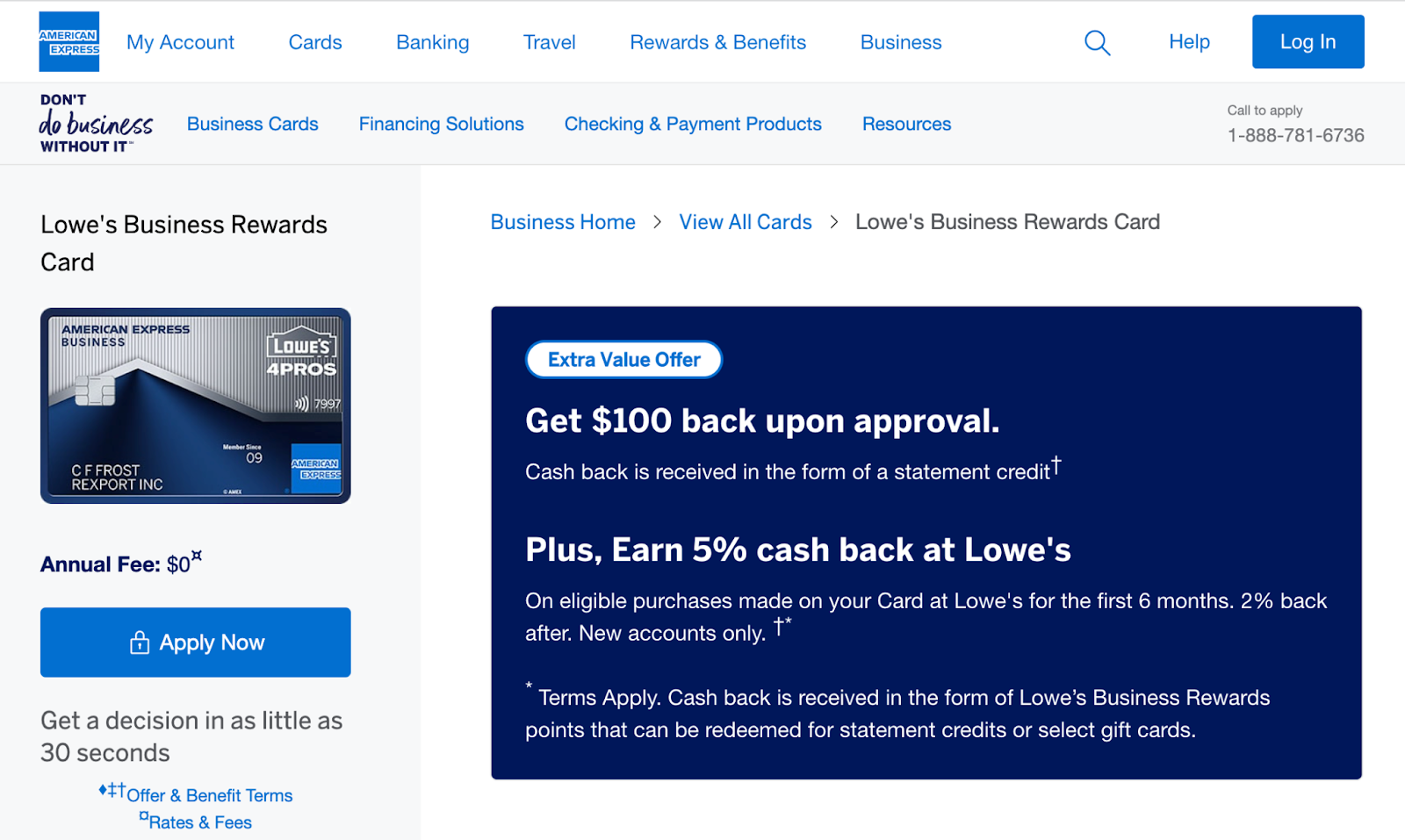

Lowe’s Business Rewards Card from American Express

Source: American Express

As its name suggests, this is another business credit card from American Express that’s heavy on rewards and is great if you shop at Lowe’s rather than Home Depot.

Here’s an overview of what you get with the Lowe’s Business Rewards Card.

For starters, you earn 5% cash back on eligible purchases at Lowe’s for the first six months (new accounts only).

While it won’t likely be a good fit if you buy your supplies from Home Depot, this card is perfect for contractors who primarily shop at Lowe’s, and you can score some serious cash back right off the bat.

After the six months have passed, you earn 2% cash back moving forward on eligible purchases at Lowe’s and 2% cash back “at U.S. restaurants, U.S. office supply stores, [and] wireless telephone services purchased directly from U.S. service providers.”

For all other purchases, you earn 1% cash back.

Source: American Express

There’s no annual fee, and as for interest, the Lowe’s Business Rewards Card from American Express has a variable 18.74 – 27.74% APR.

If it’s on the lower end toward 18.74%, that’s quite good. But if it’s on the higher end closer to 27.74%, that’s, admittedly, a little steep.

So if you choose this card and get a higher APR, you’ll definitely want to stay on top of payments and never be late.

One last thing to mention is that this card gives you benefits with Lowe’s ProServices, where you can get perks like discounted delivery and bulk rate pricing.

The bottom line is that if Lowe’s is your preferred store for contracting supplies rather than Home Depot and you want big rewards, this may be the best credit card for you.

The Plum Card® from American Express

Source: American Express

This is one of the more unique business credit cards, as there’s no interest rate.

Rather, you’re required to pay your entire balance by the end of each billing cycle.

The Plum Card® from American Express has some of the most flexible payment options.

And when using this card, you earn unlimited 1.5% cash back on the balance you pay within 10 days of the due date.

So if you paid $5,000 within the 10-day period, you’d earn a $75 credit the following month.

Otherwise, if you don’t pay by the due date, you’ll receive a late fee of “$39 or 1.5% of the past due amount, whichever is greater. If you do not pay for two billing periods in a row, the fee is the greater of $39 or 2.99% of the past due amount.”

You can get a full overview of terms, conditions, and penalties here.

Besides the hearty rewards, the Plum Card has no preset spending limit. While this doesn’t mean unlimited spending, this gives you plenty of flexibility, and your purchasing power can increase if you consistently make payments on time and maintain a good credit score.

While the $250 annual card membership fee, slightly confusing rewards, and potential to get in over your head financially aren’t ideal.

This can still be a good card for the right contractor—mainly those who don’t want any preset spending and plan on always making your credit card payment within 10 days of the due date.

How We Chose These Cards

We created this list of best credit card options for a small business owner based on these key factors:

- Introductory APR

- Regular APR

- Fees like an annual fee, balance transfer fee, and credit card processing fees

- Rewards

- Payment processing time

Cards like the Business Platinum Card® from American Express have considerable fees like a $695 annual fee, but has amazing rewards.

Others like Blue Business Cash have smaller but respectable rewards with no annual fee and 0% APR for the first year.

Each credit card has its pros and cons. But when you look at the big picture, all of these credit cards can be potentially good options for contractors and can provide the cash flow needed to fuel growth.

Each card also comes from a reputable credit card company that can, in some cases, help you build personal credit.

Note that if there’s an issue that’s preventing you from getting a credit card such as poor personal credit or a low credit score, there are several credit card alternatives that can give you access to more cash flow.

Beyond that, you may want to consider a second chance credit card, debit card, or business loan.

Wrapping Up

We listed several business credit cards that are great for contractors.

It just boils down to identifying what you’re after with rewards, interest rates, fees, and so on, and using your card responsibly.

That way you can keep the capital flowing while also building your credit score.

Also Read:

- The Best Second Chance Credit Card with No Security Deposit

- How to Use a Credit Card to Build Credit

- If I Pay Off My Credit Card in Full, Will My Credit Go Up?

- Choosing Between a Credit or Debit Card for a Teenager Simplified

- The Best Credit Card Alternatives in 2023

- The 10 Best Virtual Credit Cards in 2023 | Digital Honey

- Credit Cards for Bad Credit [No Deposit Needed]

Nick is an author, small business owner, and finance/digital marketing writer. He’s been covering the industry for over a decade and loves exploring topics to help other small businesses succeed. You can connect with him at Nickmannwrites.com.