We recommend products that we love. When you buy through links on our site, we may earn an affiliate commission.

Most know that personal credit scores affect your ability to get a loan or rent an apartment.

But some may not know that businesses have credit scores as well.

Navigating today’s business landscape relies on having excellent, all-around credit.

Many businesses rely upon their credit to secure financing as they scale. Whether you need a short-term loan or a business loan to get you off the ground, your credit matters.

Let’s take a closer look at credit scores for business loan requirements to determine where you stand.

What Credit Score Do You Need to Get a Business Loan?

Choosing to start your own business can be a lucrative endeavor.

But unless you’ve saved enough cash to bring your vision to life, you’re going to need funding.

This will likely come in the form of a business loan.

Before you have a business and can build business credit, you’ll first have to use your personal credit score to secure a loan.

But what score is going to help you make your business idea a reality?

It depends on a number of factors.

Generally speaking, a higher credit score is going to open up far more doors than a lower one will.

A high credit score says to institutions that you’re reliable and pose less of a risk of defaulting if they lend you money.

However, not all institutions will require the same credit score.

Some may require a score of 700 or higher in order to secure a loan.

Others may be more lenient and start somewhere in the mid-600s or even 500s to help you secure a loan.

Get familiar with the type of institutions you want to work with, their interest rates, and the requirements they have. This will be a helpful and essential first step to starting your business.

Which Credit Score Is Usually Used by Lenders?

Again, this is highly dependent upon where you’re at on your business journey.

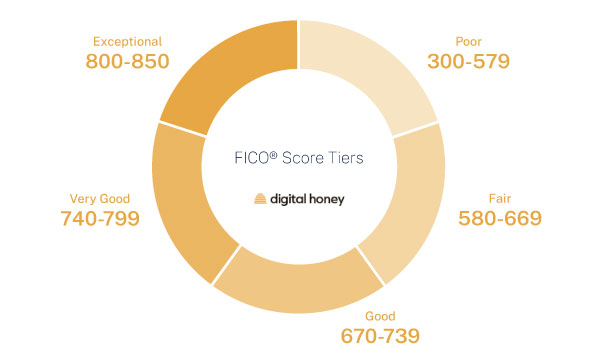

If you’ve yet to start your business because you haven’t secured funding, it will be your personal FICO credit score.

Accessing your FICO credit score is quite simple, and there are a host of services out there that can provide you with it. You can also reach out directly to agencies like Equifax or Experian.

With this in mind, you may also be a business owner who needs additional funding to grow your business.

In this case, your business credit score may be the determining factor in loan approval if you have a new business.

Whereas your FICO credit score has a consistent range, business credit scores operate a little differently.

Major credit agencies like Dun & Bradstreet, Equifax, and Experian offer different scores and ranges. That being said, the more popular range is measured anywhere from 0-100.

The higher your business credit score (80+), the more likely it is you’ll secure the financing options you desire.

In some instances, loan providers may actually consider both your consumer and business credit scores.

A good rule of thumb to follow is to make sure all your credit is up to par so that you can navigate your financial needs with confidence. (Just make sure you’re not mixing them up when it isn’t necessary as this can put you in a precarious financial situation.)

Credit Score Requirements for SBA Loans

Small Business Administration (SBA) loans are some of the most popular forms of financing. Keep in mind that these are traditional business loans offered by banks. The SBA guarantees them; it doesn’t lend.

If you’re a new prospective business owner, they’re likely going to base their decision on your personal FICO Score.

In order to secure an SBA loan, you need to have a credit score of 680 or higher. This number can vary by lender, but 680 is a good rule of thumb.

Their interest rates are excellent. For example, they can start with their base rates plus just 2.25% for $50,000 or more.

Businesses that are eligible for loans with the SBA need to:

- Operate for profit

- Be in the U.S. or its territories

- Heave reasonable owner equity to invest

- Use alternative financial resources including personal assets before seeking assistance

Different SBA loan programs have different requirements. The most popular one is the SBA 7a loan program.

According to the SBA, these are the FICO SBSS scores required for the following programs:

- 7a Small Loans: 155

- Community Advantage: 140

- Express Bridge Loan Pilot Program: 130

The FICO SBSS score is business credit score, not a personal one. It ranges from 0-300, and is primarily used to underwrite SBA loans.

If your business meets these requirements then an SBA loan might be a great way for you to secure financial assistance.

Credit Score Requirements for Bank Loans

If you plan on approaching a bank or a credit union for a business loan, you can expect much stricter requirements.

Whether we’re talking about personal or business credit scores, they need to be high.

FICO Score or VantageScore credit scores will generally need to start at 700 for a bank to consider you for a business loan.

However, this is the bare minimum needed to secure a loan.

Anything over 740 is considered the best if you want to have a better range of choices for lenders and terms.

Do you fall below 700? If so, you could always consider an alternative or work on building your credit until you’re in better financial health.

Credit Score Requirements for Equipment Financing

So far, we’ve covered the different institutions that offer loans and the scores needed to secure the best opportunities.

But while understanding the different lender types of score minimums is important, there’s something else you need to know.

There are also different types of loans you can choose to build your business.

One such loan that you might need is an equipment financing loan.

An equipment financing loan is a type of loan that a restaurant owner might need for stoves and refrigerators, for example.

The good news?

Equipment financing loans are actually quite accessible. Those who need equipment financing loans can secure one with a credit score of at least 600.

They are easier to secure because these types of loans are secured. In other words, if you default on the loan then the lender can repossess the equipment.

Still, aiming for a much higher score can improve your interest terms for any loan.

Credit Score Requirements for Short-Term Loans

While short-term loans are easy to acquire, they often come with very strict terms and high-interest fees.

If you’re not careful, this can result in a major credit hit and rapidly accumulating debt that you may struggle to pay back.

Short-term loans are an absolute last resort when nothing else is possible.

These types of loans cater most to those who have lower credit scores. In fact, you can secure a short-term loan with a FICO Score of anywhere from 560 to 660. Of course, these minimums will depend on the type of short-term loan and the lender you want.

Make sure to consider all of the above before you apply!

What is a “Good” Business Credit Score?

FICO Score and VantageScore credit score ranges are well known, so you most likely know what a good personal credit score looks like.

Because of the nature of business credit scores, however, determining where you lie can be a bit more complex.

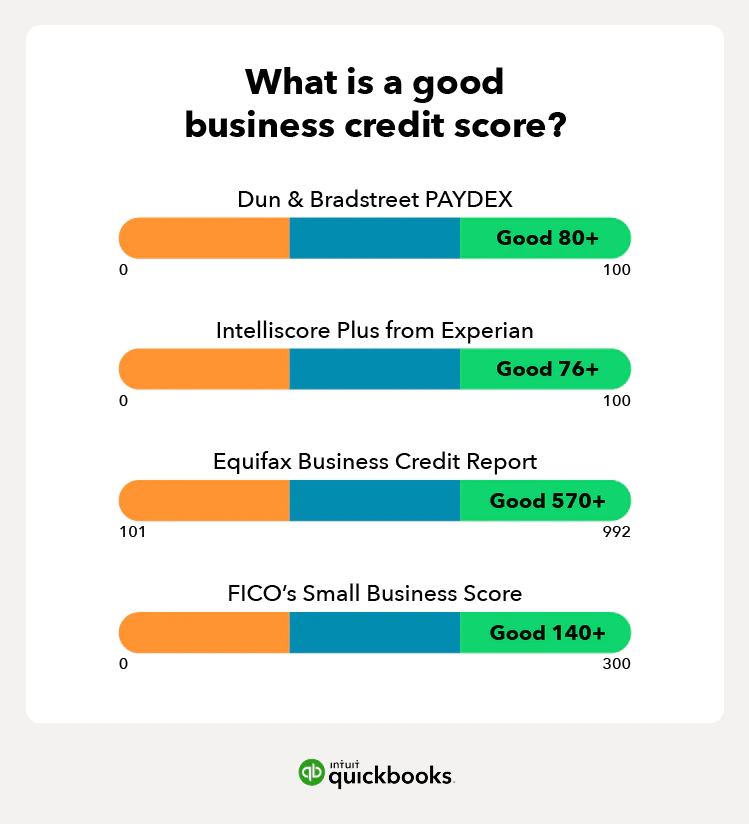

What constitutes a good business credit score depends on the agency and the scoring system used.

Source: Quickbooks

For example, let’s imagine that you turn to Dun & Bradstreet or Experian.

They use similar credit rating systems that feature a score range of 0 to 100. As a result, determining what a good credit score is can be quite simple.

If you’re anywhere from 80 to 100 on these scales, you’re a low-risk borrower with a good credit score.

But other lenders have different scoring systems.

Take, for example, Equifax. The score they emphasize most is the Equifax Business Delinquency Financial Score.

This score is designed to illustrate how close businesses may be to severe delinquency in the future. This can be helpful for newer businesses, even if it isn’t technically like other business credit scores.

The Equifax Business Delinquency Financial Score has a score range of 101 to 650 instead of 0 to 100. In this scoring system, those who have a score of anywhere from 585 to 650 have a good credit score.

There are also other credit scoring systems out there like PayNet and the Small Business Financial Exchange score.

Put simply, a good score is truly dependent upon the system that’s measuring it.

(And if your business credit is low or new, quality business tradelines help raise your business credit scores across all credit scoring systems).

However, the above is enough to give you insight into some of the most popular credit scoring systems and whether or not you have a “good score.”

A good credit score is necessary for a business loan with great interest rates.

Dylan Buckley is a freelance finance writer and editor with 7 years of professional experience. Specializing in personal finance, cryptocurrency investments, and Fintech, Dylan is deeply passionate about creating content that helps readers make informed, confident financial decisions. He studied finance in college and maintains a credit score over 780.