We recommend products that we love. When you buy through links on our site, we may earn an affiliate commission.

Almost all business credit card vendors require an SSN and an EIN when determining eligibility.

Normally, they perform a personal credit check and require a personal guarantee. But not the cards on this list.

These are corporate credit cards and gas cards that primarily want your EIN.

And while they might need your SSN for Know Your Customer (KYC) regulations, they won’t use it for personal credit checks, and there is no personal guarantee.

The Best Business Cards with EIN Only

- BILL Divvy Corporate Card

- Ramp

- Emburse Corporate Card

- Rho Corporate Card

- Airbase Corporate Card

- Phillips 66 Commercial Credit Card

- Chevron/Texaco Business Card

- Shell Business Gas Card

The Best Business Cards with EIN Only Compared

| Card | Introductory APR | Annual Fee | Welcome Offer | Rewards |

| BILL Divvy Corporate Card | None | None | None | Up to 7x on restaurants, 5x on hotels, 2x on software, and 1.5x on everything else |

| Ramp | None | None | None | Unlimited 1.5% cash back |

| Emburse Corporate Card | N/A | None | N/A | Unlimited 1% cash back |

| Rho Corporate Card | None | None | None | Up to 1.75% cash back |

| AirBase Corporate Card | None | None | None | Up to 2% cash back |

| Phillips 66 Commercial Credit Card | Prime Rate + 23.74% | None | None | N/A |

| Chevron/Texaco Business Card | N/A | None | None | Save up to $0.06 per gallon on volume-based rebates at any major fuel station with the Business Access Card. Also includes discounts on auto parts and travel. |

| Shell Business Gas Card | N/A | None | None | Save up to $0.06 per gallon on volume-based rebates, plus discounts at participating Jiffy Lube locations. |

BILL Divvy Corporate Card

The BILL Divvy Corporate Card is a business card we’ve covered before. And for good reason.

People love this card because it’s a vendor that’s eager to work with business owners and one that’s continually rolling out new features.

Right off the bat, it checks most of the boxes that business owners are looking for.

They don’t require a personal guarantee or hard personal credit inquiry. Instead, they want businesses to have at least $5,000 in monthly expenses.

The BILL Divvy Corporate Card does not report payment activity to the personal credit bureaus. But they do report to business credit bureaus, Dun & Bradstreet, and the SBFE.

It operates like a charge card, where you have to pay back everything in full within the grace period (about 30 days).

There’s no annual fee. And there are flexible rewards that are similar to Mastercard Easy Savings.

If you make weekly payments, you earn:

- 7x rewards on restaurants

- 5x on hotels

- 2x on recurring software subscriptions

- 1.5x on everything else

Note, however, that rewards are less if you pay less frequently, semi-monthly, or monthly.

You can get a full overview of the rewards program here.

The BILL Divvy Corporate Card really shines with their expense management platform. It allows employees to have cards with preset spending limits, and each expense has to be verified by the manager. Everything is recorded in their free software.

This prevents the painful end-of-month receipt and billing scramble. Plus it takes away the risk of giving employees cards!

Here’s how BILL compares with other corporate cards in its own words.

The bottom line is if you want no introductory APR, no annual fees, and great rewards without having to deal with your personal or business credit scores entering the equation and no personal guarantee, BILL is an excellent choice and a great option for spend and expense management.

Ramp

There are a lot of similarities between Ramp and BILL Spend & Expense, with both having no introductory APR or annual fee.

And both offer 1.5x cashback on all eligible business expenses (BILL offers more on restaurants, hotels, and software).

Ramp also never charges interest.

As Bankrate explains, “the Ramp Corporate Card isn’t a traditional business credit card. Rather, it’s a charge card, which means you have to pay your balance in full each month.”

In turn, you’re unable to carry a balance, which translates into 0% APR, which is a huge plus.

The main downside is that you need a minimum of $75,000 to qualify for an account opening — something that can be difficult for many small businesses.

But if you’ve got solid revenue and can maintain at least $75,000 in your business bank account, Ramp may be right up your alley.

Also, if you like straightforward rewards where you get 1.5x cash back on everything without any confusion, Ramp is a great choice.

Finally, Ramp can connect you with other lenders for business loans for additional funding.

If you’re also looking for business loans, we highly suggest Ramp, as they partner with some of the top lenders for business loans.

Emburse Corporate Card

Founded in 2014, Emburse is an up-and-comer that’s quickly growing in popularity and offers an easy-to-use prepaid corporate credit card that’s great for managing expenses.

Rather than having employees use their personal credit cards to make qualifying purchases, Emburse cards allow them to make approved purchases with each expense automatically syncing with the platform.

This gives you a bird’s-eye view of your small business finances and lets you maintain tight control of each purchase.

We like Emburse because small business owners can seamlessly create unlimited physical and virtual business credit cards for free.

And it offers unlimited 1% cash back.

While this isn’t as high as some other business credit cards on this list, it’s still decent.

That way you can stay on top of your purchases to ensure your employees are spending money on the right things while gaining access to a comprehensive expense report and earning cash back.

Note that Emburse does require a Social Security or tax ID number to verify an account, but not for a credit check — just for personal verification.

Rho Corporate Card

From the second you land on the Rho corporate card page, it instantly says “no personal guarantee or personal credit check required.”

There are also no fees.

In Rho’s own words, there are:

- No platform fees

- No cost-per-card fees

- No annual fees

- No interest

- No foreign transaction fees

- No ACH fees

- No domestic wire fees

- No international fees

- No check fees

- No Accounts Payable fees

So that’s definitely something for a small business owner to get excited about.

As for membership rewards, you earn 1.75% cash back if you pay your balance off daily.

Otherwise, you earn 1.5% cash back if you pay it off every 30 days and 0.75% if you pay it off every 45 days.

If you wait until the maximum of 60 days, you don’t earn any cash back.

Besides that, Rho lets you easily create physical or virtual cards, add Apple and Google Pay as payment options, track spending in real time, and automate expense management.

This makes Rho a rock-solid credit card issuer with business credit cards that do not report personal credit or require a personal guarantee.

So no worries if your credit score is less than perfect.

Airbase Corporate Card

A quick glimpse at Airbase, and you can tell it’s got some strong selling points.

For starters, there’s no personal credit check or personal guarantee.

There’s zero interest and no fees.

And it offers up to 2% cash back on all Airbase corporate cards, making it one of the best rewards programs in the market.

On top of that, Airbase offers up to 10-20x higher limits than many other corporate business card vendors, which is ideal if you plan on scaling up and need access to increasing amounts of cash.

In terms of the cards themselves, you can create physical and virtual cards.

You can also use Airbase to monitor purchases and set hard limits on how much employees can spend.

And if you ever need to change employee spending limits, you can do so conveniently for maximum budget control.

Finally, Airbase corporate credit cards integrate with accounting software like QuickBooks Online, Xero, and Oracle Netsuite so you can sync with your general ledger.

When you combine the simplicity, lack of fees, lack of personal credit check, no personal guarantee, and big rewards, Airbase is one of the best credit card options for small business owners.

Phillips 66 Commercial Credit Card

While not always easy to obtain if you’re a brand new company, you should be able to qualify for most business gas cards once you have a little bit of business credit under your belt. Gas cards are considered tier 2 business credit vendors.

Therefore, if you have an adequate business credit score, you’ll often be eligible for a business gas card without a personal credit check or personal guarantee.

The main benefits of the Phillips 66 Commercial Credit Card are that there’s no annual fee and it can be used at any Phillips 66, Conoco, or 76 gas station.

Also, using this card makes it easy to manage your account because you can access your bill anytime, get alerts about account activity, enroll in autopay, and more.

In terms of APR, the Phillips 66 Commercial Credit Card currently sits at 23.74% which is okay but not great.

For comparison, that’s just under 4% less than the average business credit card APR of 19.82%.

But as long as you use the card responsibly and promptly pay it off, it can be useful.

Note that it’s very cryptic about rewards for the commercial card, and you’ll need to apply to see what rewards you’ll get.

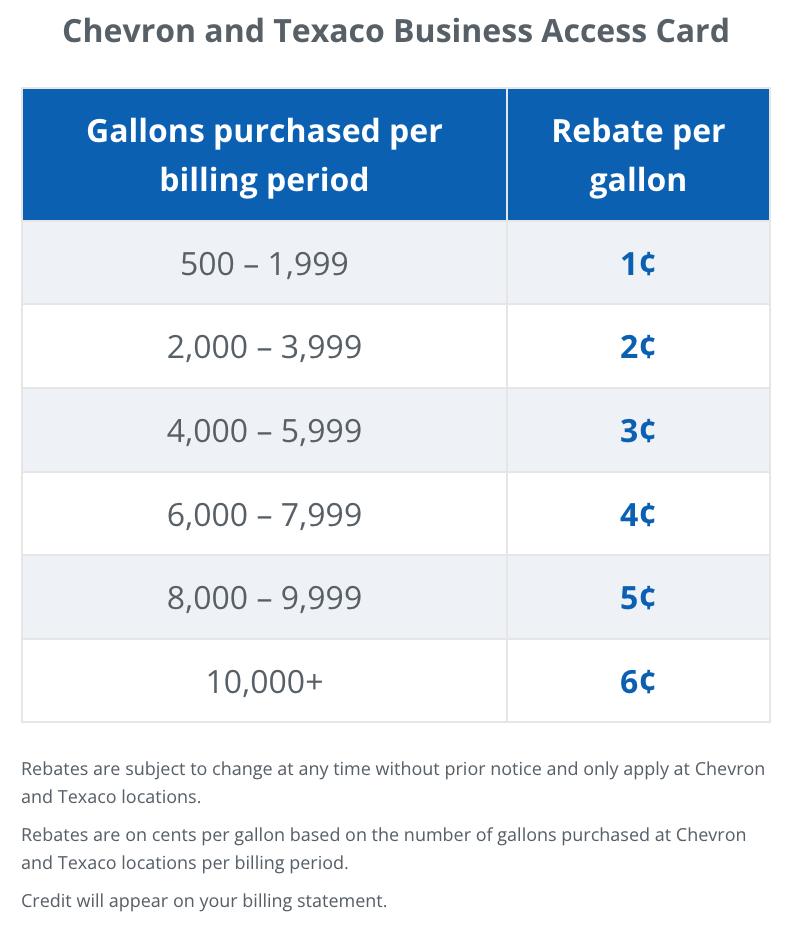

Chevron/Texaco Business Card

Let me start by saying you can only qualify with an EIN if you have good business credit.

Otherwise, you likely won’t be eligible for a Chevron/Texaco Business Card.

But as long as you have a solid business credit history, you can take advantage of this gas card.

More specifically, you can save up to $0.06 per gallon on volume-based rebates at any major fuel station with the Business Access Card, as well as get discounts on auto parts, travel, and more.

Here’s how the volume-based rebates break down.

Note that the rewards are slightly less if you use a Business Card as opposed to a Business Access Card where you only save $0.05 per gallon at Chevron and Texaco locations.

You can see a full comparison of the two cards here.

We also like that there are no set-up or annual fees with this business card, and it offers built-in account management to conveniently monitor your spending and bills.

In terms of APR, no information is provided on the website, and you’ll need to apply to see what they’ll offer you.

Shell Business Gas Card

Again, like most gas credit cards, you’ll only be able to qualify for the Shell Small Business Card if you have good business credit.

The main thing we like about this card is that you can save up to $0.06 per gallon, which can have a big impact if you operate a lot of vehicles.

We also like that this is the world’s most widely accepted fuel card, which provides your business with access to countless locations.

Besides gas, this card also covers “vehicle washes, lubricants, food, and services on the road – such as road tolls, ferry payments, and tax support.”

So if you’re looking for an “all-in-one” card that runs the gamut, the Shell Business Gas Card is one of the best. If you ever need a personal credit card for gas, they have that as well.

Beyond that, the Shell Fleet Hub makes it simple to manage your company’s fuel expenses, allowing you to track and control everything from a single dashboard.

As for negatives, Shell doesn’t disclose its APR on the website. And while it’s confirmed that there is no annual fee, Shell doesn’t provide any information on other fees like a balance transfer.

So if you’re looking for transparency, that’s not ideal.

FAQs

Can You Get a Business Credit Card With Only an EIN?

Typically, no. Even business owners with a good credit history will still need to provide an SSN and other tax ID information to apply.

That said, there are several credit cards for small business owners that won’t run a personal credit check and don’t require a personal guarantee.

They simply need your SSN for Know Your Customer (KYC) regulations to protect against money laundering and other types of fraud.

In other words, you can apply for a small business credit card without your personal credit score being a factor.

How Do EIN-Only Cards Determine Your Credit Line?

A credit card company will determine your credit line based on your income or spending within their platform.

As you prove your trustworthiness by paying your bills on time, you can build business credit and increase your credit limits.

Also, note that some companies like Ramp offer additional services like a small business loan or a business line of credit for more opportunities to generate additional cash flow. Some also offer gift cards.

Do Normal Business Credit Cards Allow EIN-Only Applications?

No. They still require personal credit checks.

For example, Capital One, Chase Ink, American Express, TD Bank, and Bank of America business credit cards always require a personal check, even if they don’t report to a personal credit bureau.

Capital One is very explicit about that as one of their factors when reviewing a business credit card application.

There are, however, several business credit cards that don’t look at your personal credit history or require a personal guarantee.

That way bad credit or a poor personal credit score isn’t an issue like it can be with traditional banks like Capital One that offer a secured credit card.

Those are the cards we focus on in this post.

Also Read:

- 5 Startup Business Credit Cards with No Credit

- 5 Secured Business Credit Cards That Report to D&B

- Ramp vs Brex: Which Is Better?

- BILL Divvy Corporate Card Reviews: Is It Right for Your Business?

- Business Credit Cards vs. Personal Credit Cards

Nick is an author, small business owner, and finance/digital marketing writer. He’s been covering the industry for over a decade and loves exploring topics to help other small businesses succeed. You can connect with him at Nickmannwrites.com.