We recommend products that we love. When you buy through links on our site, we may earn an affiliate commission.

Credit reports are usually very confusing to read! Our guide is the only one on the internet that breaks it down step-by-step. Thus making it easier for you to understand your credit report and use it to your advantage.

Each Credit Bureau’s Report Is Different

At first glance, comparing your credit reports from the three major credit bureaus might raise a few red flags. Mainly because the information reported to one credit bureau might not show on another credit bureau. You might think something is wrong here, but it’s likely not.

Creditors and lenders simply don’t report your credit history to all credit bureaus. Some of them do, but not all. So you might see a credit card account reported to Experian and TransUnion, but not Equifax. Or a personal loan only reporting to TransUnion.

That’s why it’s important to take advantage of your free annual credit reports from each credit bureau to verify your credit history. You can gather all three at once by visiting AnnualCreditReport.com. There, you can get a free copy of your annual credit report.

You could also go straight to the source with credit reporting from Experian, TransUnion, and Equifax. These are all free credit reports as well, but there are subscription-based options too.

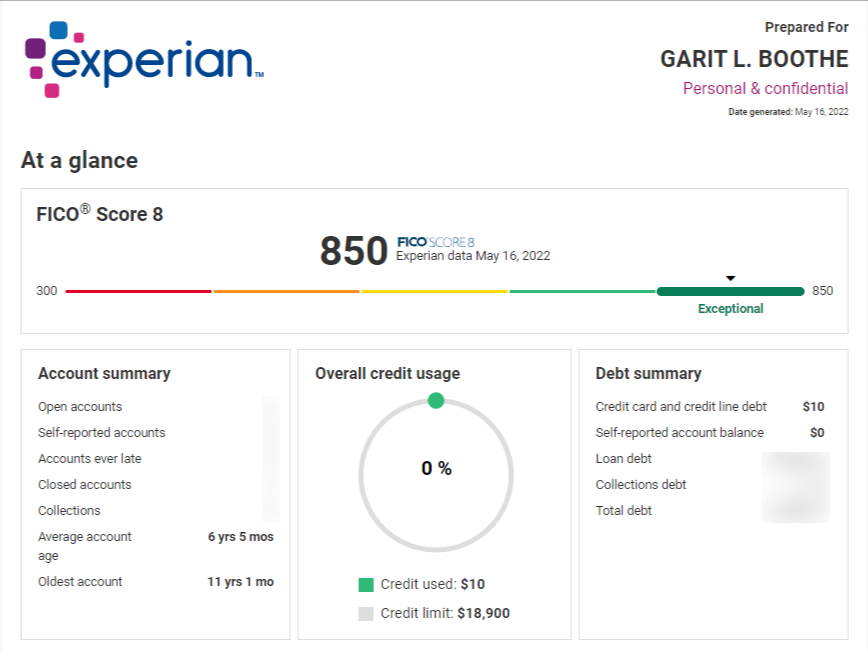

At Digital Honey, we really like Experian because it’s easy to read, and it gives you a free FICO credit score to go with your credit report! Most of the screenshots in this article are taken from an Experian credit report.

To avoid confusion when you’re combing through your credit reports, here’s a pro tip:

Make a list of all your debts and credit accounts and their balances before you do your credit report deep dive. From there you can check them off as you review each one for accuracy.

Sections of a Credit Report

There are five major sections on your credit report. Each one serves to confirm your identity and record your credit decisions. Overall, the information in these sections provides your credit history details and can even be used to guide you in fixing bad credit.

When reviewing your credit reports, you’ll need to look over each section carefully and ensure all the information is correct. Not only could false information impact your credit score, but it could also be a sign of identity theft.

If you find inaccurate information, you can start a dispute with the credit bureau to have it removed, updated, or corrected.

Personal Information

Your personal information is exactly as it sounds – the identifying information that’s specific to you. Things like:

- Name

- Address

- Employment history

- Contact information

- Social Security number

You’ll see your name and any previous names you’ve used to obtain credit. Most times, this includes your maiden name or married name. Sometimes even a misspelling might make its way through. You’ll also see previous addresses and parts of your employment history.

If you notice incomplete employment history, there’s no need to worry. It’s not meant to be a resume. Just an extra piece of identity verification. The same thing goes for addresses, although you should verify that all the addresses in your credit file are correct.

If you see unfamiliar addresses in your credit report, this could be a sign of identity theft. Also check out our article, Best Net Worth Tracker to see what your net worth might be.

Another piece of personal information used is a partial Social Security number. Usually, credit bureaus don’t include your full Social Security number as a privacy measure, but you’ll be able to verify at least the last four digits.

Credit History

Your credit history is the main show. It lists all your credit accounts along with the cold hard facts for each. Under each credit card, student loan, mortgage, and auto loan on your credit report you’ll find the following information:

- Account number (This is usually just a partial number for security reasons.)

- Account status

- Credit limit or loan amount

- Monthly payment

- Current balance

- Payment history

- Loan term

This is what potential lenders pay attention to. It’s also the key to earning good credit. Once you know where the problem is, you can pinpoint the solution to fix it.

The accounts reported on your credit history stay on for seven to ten years. Whether your account is in good standing or you’ve defaulted on a loan, both are going to be there for a while.

The accounts found in this section have a variety of statuses listed. The most common account statuses are:

- Current– Good Job!

- Late payment– 30, 60, 90, 120, or 150 days late

- Open

- Paid– Also good

- Closed– Can be closed by you or the creditor

- Transferred

- Refinanced

- Foreclosed– Only for mortgages

When you’re scanning your credit history, there are often abbreviated company names on each report. You might even see the name of a parent company instead of the one you applied with. A quick Google search often gives you some answers for what you’re looking at.

Why do companies make it so complicated to understand what’s on your credit report? Not all of them are purposefully making things confusing. However, other companies benefit from you giving up on correcting errors and inaccurate information.

Don’t let them win. Scrutinize each account on your credit report to make sure it belongs there.

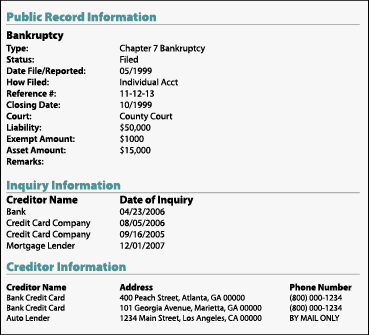

Public Records

Bankruptcies, foreclosures, and repossessions are public records that will show in this section of your credit report. They stay on your credit report for seven years, just like your credit history items. The exception to the rule is Chapter 7 bankruptcy, which stays on for up to ten years.

Here’s the problem with having public records on your report. They’re a serious red flag for lenders. It shows a pattern of delinquency on your accounts. And it’s well beyond a few late payments.

This is months of missed and late payments until your creditor decides to reclaim the asset you were supposed to be making payments on. If you find a public record that doesn’t belong to you, it’s best to file a dispute with the credit reporting agency.

What you won’t see in public records are:

- Speeding tickets

- Tax liens

- Civil judgments

- Unpaid gym memberships

A few short years ago you would have seen tax liens and civil judgments on your credit report. As of 2018, all credit bureaus removed tax liens from credit reporting. If you manage to find one on your credit report, you should dispute it.

If the public record is supposed to be on your credit, it may be helpful to issue a consumer statement. This allows you to briefly explain the circumstances behind negative information.

Here’s the good news: public records have a much smaller effect on your credit scores after two years. If you have really bad credit, start rebuilding it now!

People who diligently rebuild their credit after a bankruptcy can qualify for many types of loans and credit cards after just two years.

Credit Inquiries

Your credit inquiries come in two forms. Hard inquiries and soft inquiries. Both are used by financial institutions to assess your creditworthiness. But one of them affects your credit score and one doesn’t.

Hard credit inquiries are used to check your credit when applying for a new loan or revolving credit. Your permission is needed to run a hard credit check. These stay on your credit report for two years and can lower your credit score by one to five points.

A large number of hard inquiries can signal a higher potential risk for lenders. So borrowers should reserve their hard credit pulls for the credit accounts they truly need.

Soft inquiries don’t affect your credit at all. Many banks and credit unions do a soft pull on your credit to pre-qualify you for credit card and loan offers. Your permission isn’t needed for this one. So no matter how many soft credit pulls you do, your credit score won’t budge.

Potential Errors Worth Disputing

According to a study in January 2021 by Consumer Reports, more than one-third of consumers experienced errors on their credit reports. An error on your report could mean the difference between getting approved for new credit and getting declined.

It could also mean you’re paying a higher interest rate than what you’d qualify for if the error wasn’t there. Don’t let confusion around how to read a credit report stop you from disputing errors that have a tangible impact on your life.

Under the Fair Credit Reporting Act, it’s your right to dispute incorrect information. If you find any errors, the Consumer Financial Protection Bureau (CFPB) has a detailed guide on how you can dispute inaccurate information under each credit bureau.

Here are the most common errors you should look for in your TransUnion, Experian, and Equifax credit reports.

Incorrect Personal Information

Sometimes incorrect personal information can be harmless and does not affect your actual credit score. Other times, it can be a big sign of identity theft that you’ll need to correct right away.

If you notice parts of your personal information that are inaccurate, be sure to check the rest of your credit report for accounts you don’t recognize. Telltale signs of identity theft in this category look like addresses you haven’t lived in or unrecognizable contact information.

For incorrect personal information found on your Experian or Equifax credit report, you may have to dispute via snail mail. Correcting names can be a security risk, so they’re not disputable online.

Accounts That Don’t Belong To You

This is a huge red flag! If you review your credit reports and find accounts you don’t recall opening, you have to act quickly. Many times, identity thieves will attempt to use your credit as fast as possible to get as much as they can before you catch it.

If you come across this situation, it’s important to do a credit freeze to stop any other fraudulent activity and protect your FICO score.

Once you’ve stopped the thief from using your credit score for anything else, you should file a dispute with each credit reporting agency for fraudulent accounts. Oftentimes, this will trigger complimentary credit monitoring to protect you in the future.

Negative Items That Should Have Fallen Off, But Didn’t

This is a common issue. Even though old collections, evictions, late payments, and foreclosures should be automatically removed after seven years, it doesn’t always happen without some extra legwork. And a lot can change in seven years!

Having old debts affecting your FICO score doesn’t give lenders an accurate representation of your current credit habits. If you have a negative item hanging out on your credit report for over seven years without falling off, you need to file a dispute.

Like I mentioned earlier, the only exception to the seven-year rule is a Chapter 7 bankruptcy, which stays on for ten years. Make sure to include information about when negative items were closed and any supporting documentation to get them removed.

Duplicate Entries

This is one I experienced personally and it was such a detriment to my credit score until I got it removed. Duplicate entries hit your credit in a few different ways:

- It skews your credit utilization ratio.

- Increases your debt to income ratio.

- If it’s a negative account status, there’s a double hit to your credit score.

The first thing I did was check to make sure both entries were the same account number. They were.

Then I checked both balances to find the amounts were the same for both. The payment history, loan amount, and opening date are all checked out. So there was just one thing left to do.

I gathered my supporting documents and was able to place a dispute online. Within about two months, the duplicate account was removed and my credit score was much healthier.

Closed Accounts Listed As Open (Or Vice Versa)

You might think you’re out of the woods once you’ve closed an account, but the status isn’t always reported correctly. Accounts can be reported as still open, which may result in some mistakes affecting your payment history as well. This is completely disputable.

You could also see the reverse happen when an open account is listed as closed. This can cause a dip in your age of credit history or impact your available credit. It might also be stripping away valuable on-time payment history for that account.

Be sure to dispute either of these items as quickly as possible to limit the effects it has on your credit score.

Learning how to read your credit report is a skill that takes some practice to learn for most people. It allows you to act as your own advocate when correcting mistakes on your credit report – a service that some pay hundreds of dollars for.

You don’t have to be a credit expert to understand your report though. Experian offers credit reporting that’s easier to understand than other credit bureaus in my experience. It even allows you to access all three credit bureau reports and FICO scores at once.

Start reviewing your Experian credit reports today and put yourself on the path to better credit.

FAQs

What Are the Codes on a Credit Report?

The codes seen on your credit report will vary depending on the credit reporting company. Each one has their own guide to what their specific codes mean. In-depth code guides for each credit bureau are found here:

Can Someone Run a Credit Report Without Me Knowing?

Yes, they can. They can do this by doing a soft credit inquiry (doesn’t affect your credit) or by someone using your credit information without your permission, aka identity theft.

In the first option, it’s likely a financial institution trying to qualify you for a credit account.

With the second option, you’ll need to place a credit freeze. Avoid this by setting up credit alerts through each credit reporting agency or using a credit monitoring service.

Where Can I Find My Credit Score?

If you’re pulling your credit report from AnnualCreditReport.com, you won’t get a credit score associated with your report. Using sites like Credit Karma only provide you with an estimation of your credit score. Get the most accurate credit score information instead.

We recommend Experian for your free FICO score 8 from each bureau. If you want to pay for all of your FICO scores, go directly to myFICO.com for about $30/month.

Seychelle is a Maryland-based personal finance writer and business owner. She’s passionate about helping others out of financial pitfalls she’s already dug herself out of. Most of her finance knowledge stems from her career as a Financial Consultant and Branch Manager at the 7th largest US bank. Read more of her work on credit, budgeting, debt consolidation, and entrepreneurship at www.seychellewrites.com