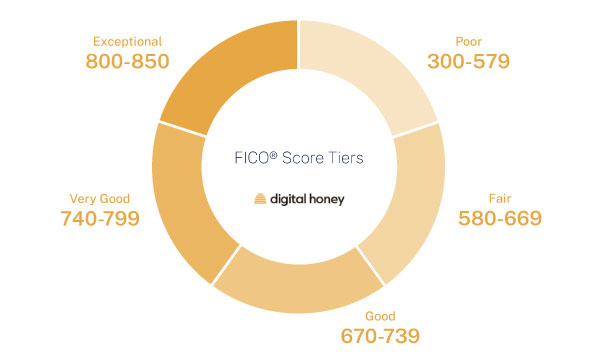

A FICO score of 580 is considered a “fair” credit score. FICO Scores range from 300 to 850 and a score range between 580 to 669 is considered “fair”. Generally speaking, a 580 score is going to limit what you can do with your credit.

580 is a “fair” credit score because this is just right above the range that is commonly considered “poor”, which is a score of 300 to 579. If you have a 580 score, then your credit report is just right on the border of where it is considered “fair” and “poor”. If you’d like to see some statistics, check out our Credit Score Statistics article on this.

Is 580 a Good Credit Score for a Mortgage?

No, 580 is not a good enough credit score for getting a mortgage. If you have a score of 580, an FHA loan is your best bet for obtaining a mortgage.

Mortgage Rates by Credit Score

| FICO Score | APR | Monthly Payment | Total Interest Paid |

| 760-850 | 4.786% | $2,252 | $380,873 |

| 700-759 | 5.008% | $2,310 | $401,757 |

| 680-699 | 5.185% | $2,357 | $418,590 |

| 660-679 | 5.399% | $2,414 | $439,153 |

| 640-659 | 5.829% | $2,531 | $481,154 |

| 620-639 | 6.375% | $2,683 | $535,751 |

From the MyFICO Loan Savings Calculator for a 30-year fixed loan of a $430,000 home, 5/14/22

580 is the score you would need in order to not have to put down a 10% down payment for a home loan. Any lower though, and you would need that much in order to qualify for the home loan.

Credit scores can change very easily based on a few factors that we will talk about later. So it would be wise to invest some time and effort into raising your credit score more so that you do not fall into the “poor” range while in the process of qualifying for a home, for example.

Also keep in mind that the higher your credit score, the better interest rates you will get.

Is 580 a Good Credit Score for an Auto Loan?

Most auto lenders use the FICO Auto Score 8 to determine creditworthiness. Its score range is from 250 to 900, so it is a little different from the FICO Score 8.

With that being said, it is only different by about 100 points, so it’s safe to say that a FICO Auto Score 8 of 700 or higher is considered a “good” auto credit score.

If you would like to obtain your FICO Auto Score 8, you can go to FICO’s website and get it and all of your other FICO scores based on a credit bureau of your choice for $19.95 a month.

You can also take a look at the table below for a closer look at average car loan rates by credit scores.

Average Car Loan Rates By Credit Range

| FICO Score | APR | Monthly Payment | Total Interest Paid |

| 720-850 | 4.037% | $678 | $2,538 |

| 690-719 | 5.351% | $696 | $3,392 |

| 660-689 | 7.751% | $729 | $4,987 |

| 620-659 | 10.403% | $767 | $6,801 |

| 590-619 | 14.759% | $831 | $9,901 |

| 500-589 | 16.272% | $854 | $11,011 |

From the MyFICO Loan Savings Calculator for a 48-month new auto loan of a $30,000

Are the differences in interest rates according to credit scores enough for you to postpone buying a car just yet? Or is the need great enough that you’re willing to do whatever is necessary?

If you feel that your credit is not good enough to qualify for the vehicle loan of your dreams with good interest rates, then take the time to improve your credit.

Is 580 a Good Credit Score for a Credit Card?

580 is not a good credit score for a credit card. Typically, credit card companies use the FICO Score 8, so a score of 580 would be considered “fair”. Most credit card companies don’t want to work with someone who has “fair” credit.

With that being said, you may qualify for the following credit cards:

You may also qualify for secured credit cards. Secured credit cards are where you put money down with the issuer as collateral in case you become delinquent on your payments.

Because of this, it makes it so that they’ll be more likely to work with you.

How To Improve a 580 Credit Score

Although 580 is not a great credit score, it is not the worst either. Now that you have a general idea of what is involved with your credit score, here is how to improve it.

Use Our Credit Building Approved Vendors

Rebuilding your credit score takes time, but it is easier when you use our top credit-building service providers. The following services can help:

- Credit Strong: Credit Strong provides the best credit builder loans. They offer installment loans that use the monthly payments as collateral. Credit Strong reports your monthly payments to each major credit bureau which then raises your credit score. They also do not run a credit check and you can cancel your account at any time.

- BoomPay: Unfortunately, rent is often not reported to the credit bureaus, but with BoomPay you can now do so through their rent reporting services. They provide previous and current rent payments to all three credit bureaus for significantly lower costs than their competitors.

- Extra: Normal debit cards do not build credit, but with Extra you can finally do so. It’s a debit card that allows you to build credit and earn rewards like a credit card does but without requiring a credit check. (Debit Cards That Build Credit)

- Experian Boost: Experian Boost allows you to finally build your credit with your phone bills, utilities, and streaming services. They even provide you with your Experian credit report and FICO Score 8 for free.

These are ways to quickly build up your credit score. They can also help you if you have a thin credit profile.

Maintain a Good Payment History

Payment history is the biggest percentage factor of your FICO 8 Score; 35%. This is important to note because keeping a good payment history is critical to raising your credit score.

Even if you only miss a monthly payment on your credit card occasionally, it is going to be hard for you to build credit.

If you have multiple monthly payments that you need to keep track of and feel that one is going to slip through the cracks, consider setting up automatic monthly payments.

This is a fantastic way to ensure that you always pay on time and is a great way to build credit when your payment history is not that good.

Decrease Your Credit Utilization

Credit utilization, otherwise known as “amounts owed” on your FICO 8 Score, is worth 30%.

Your credit utilization ratio is basically the ratio of your credit card balance to its limit.

For example, if you have a credit card with a $500 limit and your balance is currently at $300, your credit utilization is 60%.

This is considered a very high credit utilization rate. You will want your credit utilization to be 10% or lower.

The easiest way to do this is by paying down your credit card bills and being mindful of how much you spend each month in relation to your credit limit.

Start Now To Improve Your Credit History

There is no better time to start improving your credit history than right now.

If you are ready to make a change, take advantage of the tools and services above to help you improve your credit score.

If you are not ready to use these services, do not worry.

You should still start paying your monthly bills on time and be mindful of your credit utilization.

Even if you can only do one of these things, it is a great way to begin an upward trend when it comes to your credit score.

Start now to improve your credit history.

FAQs

Can I Get Approved With a 580 Credit Score?

You can get approved for certain types of loans with a 580 credit score. However, it is more difficult and you will pay a higher interest rate.

Some types of loans that you might get approval for are FHA loans, auto loans, or credit cards with high-interest rates.

The best advice we can give you is to wait if you can on applying for the type of loan you want and improve your credit for better terms and conditions later.

How Can I Raise My Credit Score Fast?

They say that slow and steady wins the race, and in the case of raising your credit score, this is sound advice.

That said, there are some ways that you can speed up the process of improving your credit score a bit.

If your credit is not very good, one of the quickest ways to see a boost is to open an account with the following:

• BoomPay

• Credit Strong

• Extra

• Experian Boost

Having another line of credit is a great way to improve your credit score because it shows that you are responsible and have a history of paying bills on time.

You can get a lot of value from these strategies, but they are not a substitute for making your payments on time and reducing your debt.

Also Read: