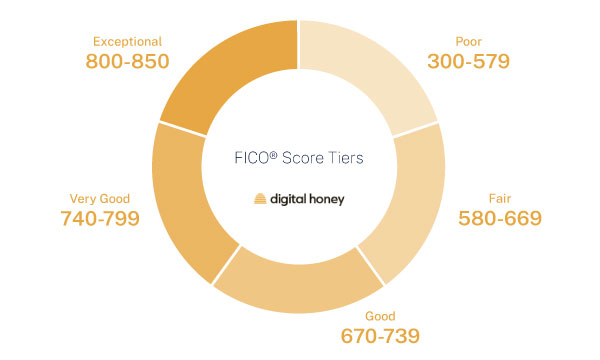

A credit score of 570 is commonly considered poor. You’ll have a difficult time qualifying for any sort of loan that requires a credit check. If you’re approved for an account, it’s likely to have a very high interest rate. The FICO Scores range from 300 to 850, with anything below 580 being branded as poor.

Is 570 a Good Credit Score for a Mortgage?

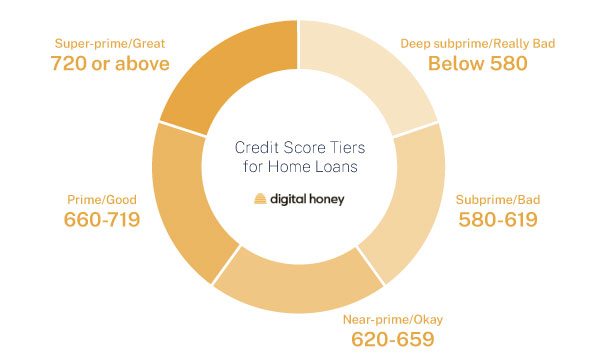

570 is a terrible credit score for mortgages. In this table, you’ll see that FICO doesn’t provide a credit score interest rate for credit scores below 620!

Mortgage Rates by Credit Score

| FICO Score | APR | Monthly Payment | Total Interest Paid |

| 760-850 | 4.786% | $2,252 | $380,873 |

| 700-759 | 5.008% | $2,310 | $401,757 |

| 680-699 | 5.185% | $2,357 | $418,590 |

| 660-679 | 5.399% | $2,414 | $439,153 |

| 640-659 | 5.829% | $2,531 | $481,154 |

| 620-639 | 6.375% | $2,683 | $535,751 |

From the MyFICO Loan Savings Calculator for a 30-year fixed loan of a $430,000 home, 5/14/22

If you have a credit score of 570 or below, an FHA loan is your best bet for obtaining a mortgage. A Federal Housing Administration (FHA) lender may consider loans with credit scores as low as 500 provided that you make a down payment of at least 10%.

If you can’t afford to put down 10% for a home loan, you’ll need a credit score of 580 or higher. You might be able to reach that score in a few months if you put out some effort.

If you have a terrible credit history, but your mortgage lender decides to approve your application anyway, you’ll most likely get the highest possible interest rate. Because mortgages have such large principal amounts, consider postponing your application until your credit improves.

Is 570 a Good Credit Score for an Auto Loan?

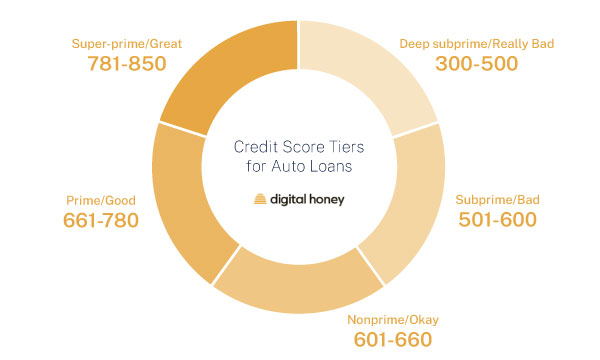

A credit score of less than 600 does not indicate a good credit score for an auto loan. A 570 credit score allows you to get an auto loan, but the interest rate will be extremely high. Auto loan principal balances may be lower than those of home loans, but their maximum interest rates are many times higher.

As a result, even if your credit score is bad, you may be spending a lot of money on excessive interest rates.

Take a look at the table below of average car loan rates according to credit score:

Average Car Loan Rates By Credit Range

| FICO Score | APR | Monthly Payment | Total Interest Paid |

| 720-850 | 4.037% | $678 | $2,538 |

| 690-719 | 5.351% | $696 | $3,392 |

| 660-689 | 7.751% | $729 | $4,987 |

| 620-659 | 10.403% | $767 | $6,801 |

| 590-619 | 14.759% | $831 | $9,901 |

| 500-589 | 16.272% | $854 | $11,011 |

From the MyFICO Loan Savings Calculator for a 48-month new auto loan of a $30,000, 5/14/22

As you can see, there’s a significant difference between the highest and lowest possible interest rates on automobile loans.

You may not be able to postpone your desire for a vehicle, but keep in mind the expenses associated with poor credit before financing your next automobile purchase. If you can invest time into improving your credit score before submitting an application, it will be worth it.

Is 570 a Good Credit Score for a Credit Card?

570 is a not a good credit score for a credit card. Your credit card applications will be denied by the major credit card companies. You will receive only limited approvals with high fees and high interest rates. Fortunately, there are a few “bad credit” credit cards that you may accept your application.

A 570 credit score is less of a barrier to obtaining a credit card than it is with other sorts of financing. If you’d like to see some statistics, check out our Credit Score Statistics article for more. You won’t be able to obtain the best credit card accounts, but at the very least you’ll be able to acquire one or two.

The following are examples of “poor credit” credit cards:

Another alternative is to apply for a secured credit card. You’ll need a cash deposit as collateral, which usually equals the card’s available credit limit.

That makes them an even safer bet for the credit card company and more accessible to borrowers with terrible credit than an unsecured credit card. You can even look into Best Credit Building Apps if you prefer to go the app route.

How To Improve a 570 Credit Score

Fortunately, there is hope for those with bad credit. You can always repair your credit if you apply yourself, work hard, and use good judgment. If you need assistance in getting started, follow the instructions below.

Use Our Credit Building Approved Vendors

Rebuilding your credit score takes time, but it’s a lot easier when you enlist the help of our top credit-building service providers. The following are the services we think you should start with:

- Credit Strong: Credit Strong offers the best credit builder loans. They’re a type of installment loan that uses the proceeds as collateral. Credit Strong’s loans are highly customizable, and they report your activity to each major credit bureau. There’s also no credit check and you can cancel at any time.

- BoomPay: Your rent payments typically don’t show up on your credit report, but you can pay to add them through rent reporting services. BoomPay is our favorite of the available options. They report previous and ongoing rent payments to all three credit bureaus for much lower fees than their competitors.

- Extra: It’s typically impossible to build credit with a debit card since they’re not credit accounts, but Extra offers a way around that. It’s a debit card that lets you build credit and accrue rewards like a credit card, but it connects to your bank account with no credit check. (Debit Cards That Build Credit)

- Experian BOOST™: Just as BoomPay reports your rent payments, Experian BOOST™ lets you build credit with the bills for your phone, utilities, and streaming services. It also lets you access your Experian credit report and FICO score. Best of all, it’s completely free.

These options can significantly speed up your credit-building process. They’re also a great way to fill out a thin credit profile.

Maintain a Good Payment History

Payment history is worth 35% of your FICO score, making it the most significant factor in their scoring model. It’s worth as much as the length of your credit history, your credit mix, and new credit on your credit report put together.

Because of this, avoiding late payment at all costs is critical to improving your credit score. Even if you only miss a monthly payment on your credit card debt occasionally, it’ll be hard to build credit.

If you have multiple monthly payments to keep track of and worry that one might slip through the cracks, consider setting up automatic minimum monthly payments. It’ll protect your credit rating and reduce the likelihood of overdraft fees.

Decrease Your Credit Utilization

One of the primary ways that lenders gauge the health of your outstanding debt levels is through your credit utilization. In simple terms, that’s the ratio between the amount you owe on an account and its total borrowing limit. For example:

- A $4,000 credit card balance on an account with a $5,000 credit limit has an 80% credit utilization ratio.

- A $5,000 balance on a personal loan with a $10,000 principal amount equals a 50% credit utilization ratio.

Paying down your debts and reducing your credit utilization ratio for your revolving credit accounts and installment debts will benefit your score tremendously. Generally, the ideal credit utilization ratio is between 1% and 10%.

Start Now To Improve Your Credit History

Whatever strategies you use, improving your credit history is a marathon, not a sprint. In other words, it takes time to get an excellent credit score, and the sooner you start, the better.

The worst-case scenario is that you start looking for a house or a car, realize you have a lower credit score than you like, and then try to improve your situation.

Much like investing, the best time to start building your credit was yesterday. The second best time to start is today. Take action now to start improving your credit history.

FAQs

Can I Get Approved With a 570 Credit Score?

Some lenders will approve you for certain types of credit with a 570 credit score. For example, you might be able to get an FHA home loan, an expensive auto loan, or a credit card for borrowers with bad credit.

However, you’ll have a much harder time qualifying for accounts than you would with a higher score. In addition, you’ll likely have much less attractive terms, such as a higher minimum down payment or interest rate.

In many cases, you’d be better off waiting to apply for significant credit accounts until you improve your credit score.

How Can I Raise My Credit Score Fast?

Raising your credit score generally isn’t something that you can rush. In fact, trying to improve your credit at the last minute before applying for a home loan or an auto loan can often backfire.

For example, if you take out a new credit account, you can add a hard inquiry to your credit report and increase your amounts owed.

That said, there are a few ways to make significant progress in a relatively short time. For example, you could:

• Report your rent, utilities, or streaming service payments.

• Become an authorized user on someone’s credit card.

• Request a credit limit increase to reduce your utilization ratio.

There can be a lot of value in these strategies, but they’re not a substitute for consistent, timely payments and sustained debt reduction.

Also Read: